** The morning has been mixed at the CBOT with the grains weaker while the soy complex firmer. The short covering in the grains appears to have slowed/ended while a few of the faster moving funds are exiting a few shorts in soybeans. Everyone appears to be wanting to “get smaller” in their exposure to the CBOT heading into Thursday’s USDA report. Traders hold a bearish mentality in the summer row crops due to seasonal considerations and prior year price performance. However, the insipid Midwest dryness that has prevailed since June could alter the seasonal price landscape. US corn, wheat and soybean stocks and stock/use ratios are both in decline – much different than recent years. The last time that an August rally evolved was back in 2012 when dryness struck the W Midwest causing reduced corn/soy yield prospects. Until there is an improved weather outlook for Midwest crops, the downside CBOT price risk appears to be limited.

** There are 61 Mil acres of US corn and soybean ground that is short to very short of soil moisture. This is nearly double the amount of farmland that was dry in the past few years with crops in IA and C IL in immediate need of rain.The cool Midwest temperatures have helped diminish crop stress, but the time has arrived for rain! Corn and soybeans in some of the drier areas of IA are rolling leaves in the afternoon – even with high temps in the upper 70’s to the lower 80’s due to a lack of moisture. The point is that unless the Central US weather pattern changes quickly to feature rain, US crop ratings and yield estimates will be in decline following Thursday’s USDA August crop report.

** China imported a record 10.1 MMTs of world soybeans in July with the crop year total pace exceeding the USDA annual forecast of 91 MMTs with just 8 MMTs needed to be taken in August and September. ARC is raising our 2016/17 Chinese soybean import pace to 93 MMTs, up 2 MMTs from the WASDE forecast. The 2017/18 WASDE Chinese soybean import forecast of 94 MMTs, would only be up 1 MMTs from the current year! It appears to be too low by 2-3 MMTs. If WASDE were to raise its 2017/18 Chinese soy import pace to 96-97 MMTs, it would have to raise 2017/18 US soybean export estimates by 25-50 Mil Bu to 2,175-2,200 Mil Bu!

** Updates from Canadian producer sources reflect a deepening and spreading drought across the Prairies. The yield losses are rapidly building. The all wheat crop estimate has fallen below 24 MMTs with canola below 18.5 MMTs.

** CBOT brokers estimate that funds have sold 4,200 contracts of wheat, 6,600 contracts of corn while buying 2,100 contracts of soybeans. In soy products, funds have bought 1,000 contracts of soymeal and 2,600 contracts of soyoil. ARC has no idea why funds turned such aggressive sellers of grain early AM?

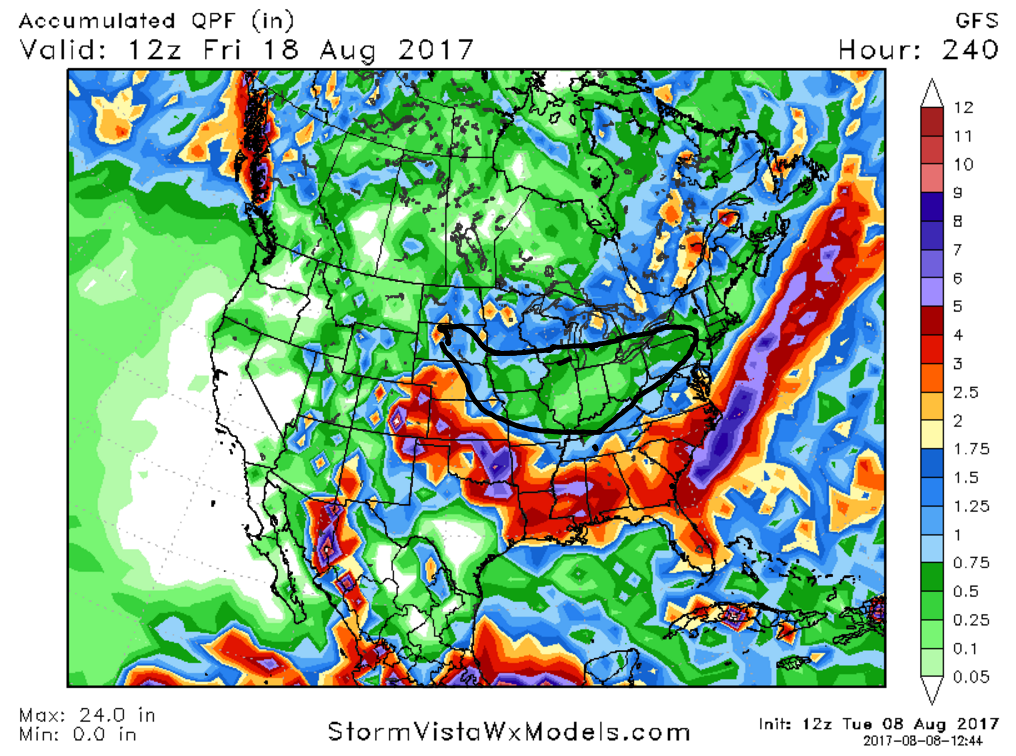

** Midday GFS Weather Model Update: The forecast is similar for the next 8 days with limited rain for the heart of the Midwest (from IA to OH). There could be a few Midwest showers of traces to .25”, but meaningful rain will occur southeast/east from Colorado into the Carolina’s – including the Gulf States! Rain totals here will range from 1-4.00” with localized heavier. Any coverage of Midwest rainfall will be less than 30%. Soil moisture levels will decline across the Midwest with crop stress rising. High temps will range from the mid 70’s to the mid 80’s with warming to occur in the 11-14 day period. A Ridge of high pressure builds northeast from the Intermountain West. The need for rain will increase with the return of warmer temperatures after August 20th.

** AgResource Market Comment: Demand for world soybeans remains astounding and USDA will raise US exports in an old crop position by 35-50 Mil Bu. Arid weather conditions for Midwest crops is causing new worry with soybeans being the crop most impacted. The downside price risk in CBOT corn, wheat and soy futures is limited amid declining US and world crop production totals. End users hope for a bearish USDA report!

** GFS 12z 10 Day Rainfall Forecast: