** ARC will release our Weekend Summary this afternoon. We wish everyone a happy and safe Labor Day weekend!

** Early fund selling in corn and a sideways trade in wheat/soybeans has been the theme at the CBOT this AM. The volume of trade has been better than expected in corn, but holiday reduced in soybeans and wheat.

There was good selling in early CBOT dealings, and then as the selling faded, the market has been able to recovery. ARC expects CBOT prices to close mixed heading into the long holiday weekend. In fact, the market may hold in a sideways mixed trade until greater clarity is offered via the September NASS Crop Report.

** CBOT brokers report that funds have sold 7,000 contracts of corn and 2,200 contracts of soybeans, while being flat in wheat. In CBOT soy products, funds have sold 3,000 contracts of soymeal while buying 2,500 contracts of soyoil.

** Informa released their September Crop Forecasts this AM with a yield of 169.5 BPA in corn and 49.4 BPA in soybeans. These yield estimates were close to trade expectations and have not had much market impact.

** Vietnam has decided to allow DDGs to be imported which will act as a drag on future soymeal imports. The news has been seen as slightly bearish to the meal market this AM. There is no way to estimate the volume of DDGs imports that will be taken in 2017/18.

** Iran has exported 100,000 MTs of wheat and there may be strong demand for any durum stocks. Iran banned wheat imports 2 weeks ago and they are expected to ship out 1-1.5 MMTs during the marketing year.

** Tunisia paid $193-193.75 for 50,000 MTs of milling wheat CIF. The price paid was close to replacement.

** Its likely to be a bumpy fall for CBOT prices as the September Crop report and US harvest yield results are awaited. The world market has plenty of supply and end users are not willing to chase the market higher. That is why that rallies like Thursday are unable to carry through.

** China has been a buyer of dips in soybeans taking and estimated 18-22 cargoes this week. However, South America remains an aggressive seller of corn with Argentine offers declining on a CBOT corn rally. It’s doubtful that either US 2017/18 corn/soybean exports came move much higher from the WASDE forecast made in August. Its supply (not demand) that will have to be the catalyst for higher CBOT values.

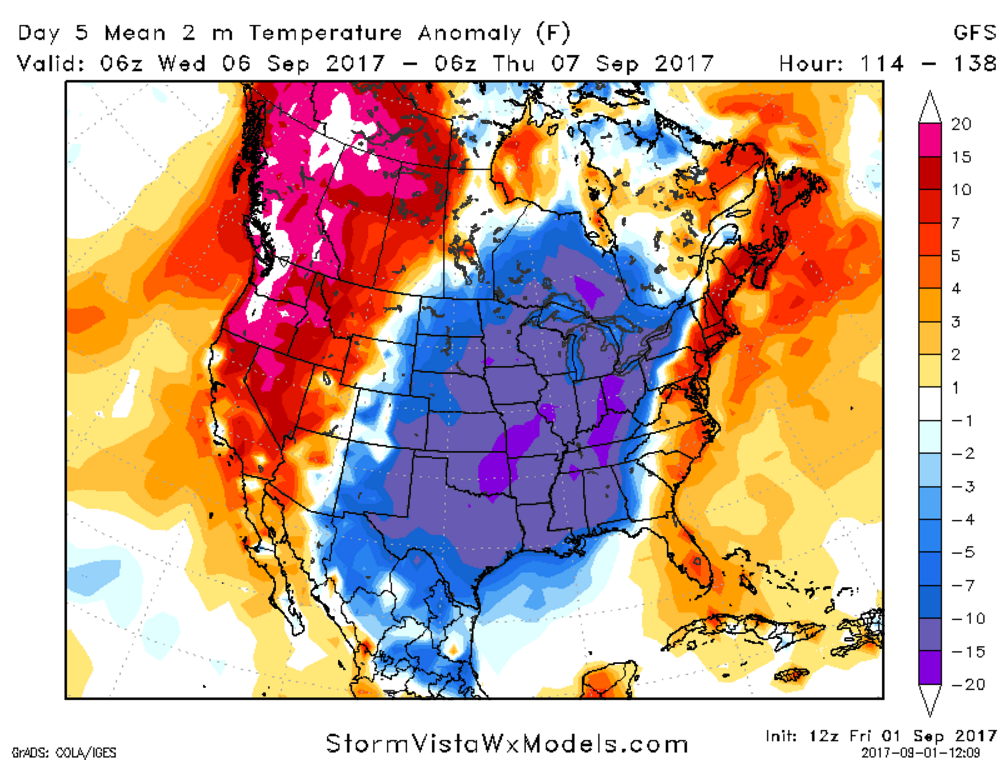

** Midday GFS Weather Model Update: The forecast is little changed at midday. The rains will continue across KY for another 12-18 hours before dry/cool weather prevails across all of the Plains and the Midwest. The GFS offers limited rainfall for Plains and the fat areas of the Midwest for the next 12 days. The midday model takes Hurricane Irma into NY, but this is just too far out for any confidence. However, our confidence is rising that Irma will not impact the Gulf and it will be an East Coast system. This will be a cat 4-5 storm and needs to be watched closely. Our hope is that Irma does not make US landfall as it’s a dangerous storm.

** AgResource Market Comment: Following yesterday’s strong chart based bounce, the CBOT has become uncertain on its future price direction? Our bet is that prices hold in a range without a major Midwest frost/freeze risk into mid September. The US corn crop needs more DGDs to reach black layer, slow corn maturity will be evident on weekly crop progress reports. Soyoil continues to be the bull stalwart on bio fuel demand and rising canola prices. Ahead of harvest, we would not chase any rallies.