** It has been a dull and listless trading session at the CBOT with corn, soybeans and wheat futures being little changed. Wheat futures have found support on lower Aussie crop estimates and rising world fob offers, while the fear of the 1st active harvest weekend caps rallies in corn and soybeans.

The volume of CBOT trade is poor and few want to take on any large new net positions amid the chop in CBOT values of recent days. ARC looks for a mixed close with some pre hedging noted in the summer row crops going home. The market lacks direction —- and a driver.

** Harvested Midwest corn and soybean yields are highly variable depending on summer and early autumn weather conditions. 90% of the producers are reporting yields below last year. The 2017 trend yield is 171 BPA in corn and 48 BPA in soybeans. The industry is trying to decipher whether the ‘17 US corn and soybean yield are 2-3% either side of that trend – difficult with just 10% of the US crop being cut to date. And even amid the expanding harvest, the debate over US yields may have to wait until NASS releases its October Crop report next month. As a general comment, producers are more pleased with their corn yields. Harvest will become much more active next week, and yield reports should become numerous, traders will grind through the data for a trend.

** The weekly US export sales report for the week ending Sept 14th were; 11.3 MMTs of US wheat (2.1 HRW, 1.1 SRW, 4.5 HRS, 2.7 Mil Bu SWW, and 800,000 MTs of durum), 20.7 Mil Bu of corn, and 85.9 Mil Bu of soybeans. The slow grain sales totals were slightly bearish while soybeans were slightly bullish. China soybean purchases are lagging last year, but sales to unknown destinations are surprisingly good.

** For their respective crop year to date, the US has sold 481 Mil Bu of wheat (down 14 Mil Bu or 2.8%), 434 Mil Bu of corn (down 272 Mil Bu or 38%), and 710.3 Mil Bu of soybeans (down 187 Mil Bu or 21%). The early sales pace of US corn, soybeans and wheat has been a poor predictor of final crop year totals.

** China halted banking operations with North Korea which offers an “olive branch” to the Trump Administration in their effort to denuclearize North Korea. The Chinese banking move will sooth trade issues as North Korea remains on the forefront of the Trump Administrations Agenda.

** Private crop analysts are lowering their Australian Wheat Crop estimates to 18.5-19.0 MMTs as dryness is really starting to take a bite on small grain yields. The USDA is pegging the Aussie wheat crop at 22.5 MMTs.

** Saskatchewan Agriculture is estimating their all crop harvest has progressed to 75% completed, the best since 2012! The spring wheat harvest is 76% finished with canola 64% cut. The oat harvest is 65% completed.

** Midday GFS Weather Model Forecast Update: The forecast is little changed from the overnight run with moderate to heavy rains slated to drop across the NW Midwest and the W Plains from a stuck Ridge/Trough pattern. 1-4.50” of rain looks to fall across; MN, SD, NE, KS and TX over the next 7 days.

The dry E Midwest will continue to see limited rainfall with active harvest expected. Rain potential for the E Midwest looks to range from .1-.6” into the end of the month. Hurricane Maria looks to hold off shore and not impact the US. Temps average much above normal with highs in the 80’s to mid 90’s for the E Midwest. Some record highs are likely this weekend.

** AgResource Market Comment: The $9.80 price is key for November soybeans as the daily chart is forming a bull flag and the 200 day moving average crosses at the same level. ARC research argues that Nov soybeans scored its seasonal low back in August, and with a seasonal buy date at October 6th, the market has to push lower over the next 2 weeks for the bears to be vindicated. Wheat has a supply story with Russian/Ukraine/Australian dryness. Corn is just a follower. ARC research calls for a choppy range trade with soybeans having the most upside potential.

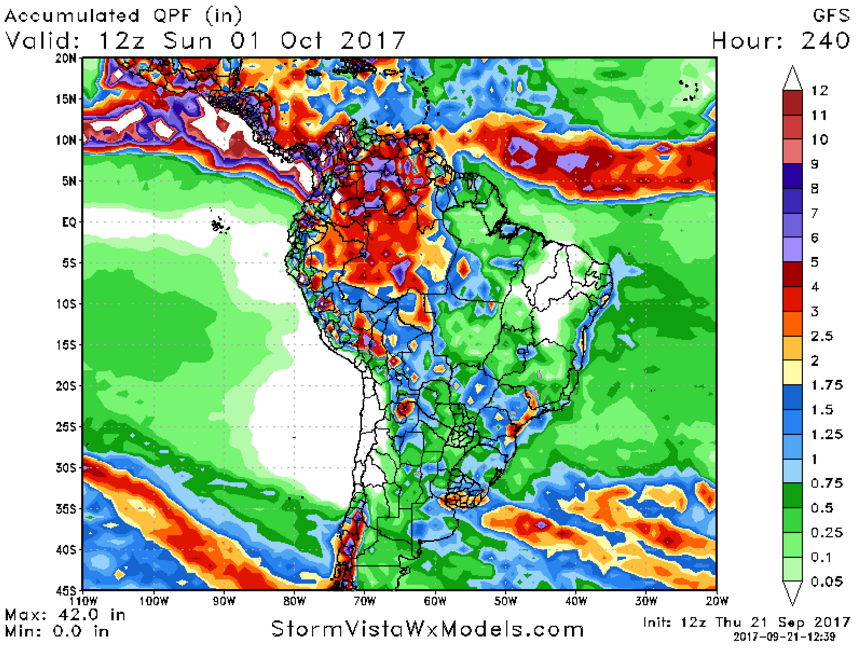

** GFS 10 Day Rainfall Forecast for N and S America;