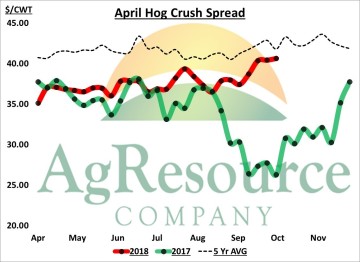

Hog feeders today are watching April hog futures, as weaned pigs that are placed today will be marketed against the April contract. April hogs bottomed in August, and this week are trading at a historically large $10 premium to the cash index, and are priced $16 higher than a year ago. The chart shows the April hog “crush” spread, or the hog feeding margin that can be locked in by selling April hogs, and buying March corn and soymeal. The spread this year is just under the 5 year average, but substantially higher than a year ago. Feed costs offered by the CBOT’s corn and soymeal markets are historically cheap, and basically unchanged from last year. However, cash hog prices are trading very strong relative to supply, while forward premiums that are priced into CME hog futures are also exceptionally rich.

Hog feeders today are watching April hog futures, as weaned pigs that are placed today will be marketed against the April contract. April hogs bottomed in August, and this week are trading at a historically large $10 premium to the cash index, and are priced $16 higher than a year ago. The chart shows the April hog “crush” spread, or the hog feeding margin that can be locked in by selling April hogs, and buying March corn and soymeal. The spread this year is just under the 5 year average, but substantially higher than a year ago. Feed costs offered by the CBOT’s corn and soymeal markets are historically cheap, and basically unchanged from last year. However, cash hog prices are trading very strong relative to supply, while forward premiums that are priced into CME hog futures are also exceptionally rich.

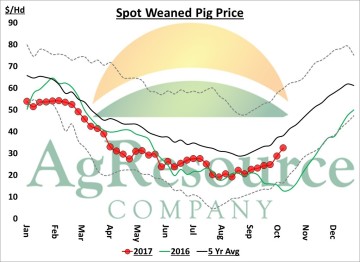

Forward feeding margins have been below average all year, but have been above a year ago through the summer, and turned higher in early September. Despite the large hog supplies, improving forward margins have carried directly back to spot wean pig values. The chart shows the weekly 10-12 Lb weaned pig spot price quote from the USDA. Last week’s weighted average price of $32/head, was nearly $20 higher than what was quoted for the same week last year.

Forward feeding margins have been below average all year, but have been above a year ago through the summer, and turned higher in early September. Despite the large hog supplies, improving forward margins have carried directly back to spot wean pig values. The chart shows the weekly 10-12 Lb weaned pig spot price quote from the USDA. Last week’s weighted average price of $32/head, was nearly $20 higher than what was quoted for the same week last year.

Assuming the USDA’s pigs/litter estimate from last quarter and current spot prices, each sow farrowed is producing approximately $340 of revenue versus $170 last year, and $377 in 2015. Farrowing intentions for Dec-Feb were at a 10 year high, but just 1% larger than a year ago. Even with record production forecast for the year ahead, the market is telling producers to increase output.

After 2 consecutive years of losses, estimated cattle feeding margins turned positive back in January, and then slipped back into the red at the end of the summer. Volatility in beef and cattle prices has remained heightened through 2017, and while production is forecast to expand in the months/quarters ahead, prices are still trading relatively strong. In fact forward cattle prices at the CME are back to incentivizing Autumn feeder cattle placements. The chart reflects the difference between buying November feeder cattle and March corn, while selling April live cattle futures. The spread has pushed to new highs for the year this week, and just slightly under a year ago. Since 2010 the spread has offered positive paper profits in just 2 other year. The September placement rate is expected at 108% of a year ago, and the CME is telling feedlots to keep placing. However, cattle feeders need to be mindful of margins and willing to lock in profitable prices when offered, as total red meat production reaches record levels in the year ahead.

After 2 consecutive years of losses, estimated cattle feeding margins turned positive back in January, and then slipped back into the red at the end of the summer. Volatility in beef and cattle prices has remained heightened through 2017, and while production is forecast to expand in the months/quarters ahead, prices are still trading relatively strong. In fact forward cattle prices at the CME are back to incentivizing Autumn feeder cattle placements. The chart reflects the difference between buying November feeder cattle and March corn, while selling April live cattle futures. The spread has pushed to new highs for the year this week, and just slightly under a year ago. Since 2010 the spread has offered positive paper profits in just 2 other year. The September placement rate is expected at 108% of a year ago, and the CME is telling feedlots to keep placing. However, cattle feeders need to be mindful of margins and willing to lock in profitable prices when offered, as total red meat production reaches record levels in the year ahead.