AgResource Daily Farm Marketing Advice for Monday: 1/Corn Producers: Sell 10% of the estimated ‘18 corn harvest at $4.01 basis Dec 2018 futures. 2/ Corn Producers: Sell 10% of estimated ‘19 corn production at $4.17 basis Dec 2019 futures. 3/ Corn Producers: Sell 15% if the 2017 corn crop is March 2018 corn futures reach $3.72.

Higher has been the morning in Chicago as fund short exit grain markets, with the soy complex in tow. There’s not a lot of fresh news at midday, but there’s a general expectation that interior US basis looks to improve as corn harvest reaches 50-55% complete, and as bean harvest surpasses 80% finished in the next two weeks.

No new export sales were announced this morning, but Morocco is seeking 30,000 MTs of Us soft wheat and 327,000 MTs of US durum via its origin quota system. Weekly US corn & soybean export inspections improved substantially on the week, while wheat shipments were rather meager.

Through the week ending Oct 19th, the US shipped 94 Mil Bu of soybeans, vs. 66 Mil last week; 24 Mil Bu of corn, vs. 13 Mil a week ago; and just 6 Mil Bu of wheat, vs. 12 Mil the week prior. Combined shipments are up 34 Mil Bu at 125 Mil, which is largely a function of improved logistics, but another several weeks of large (95-110 Mil Bu) soy inspections are anticipated.

For their respective crop years to date, the US has shipped 178 Mil Bu of corn, down a hefty 46% from last year; 361 Mil Bu of soybeans, down 8% from last year; and 397 Mil Bu of wheat, down 5%. Better US export demand is needed, but otherwise shipments to date are generally in line with USDA forecasts.

ARC expects the US corn harvest through Sunday hit 42-44% complete, with soybean harvest progress pegged at 64-65% finished.

Harvest pressure will be in retreat moving forward, and focus will shift to South America’s Nov/Dec climate pattern, which so far appears to be close to normal, but lingering dryness in parts of Central Brazil, and too much rain in La Pampa & Buenos Aires in Argentina needs close watching. ARC also notes that La Nina does look to be establishing, with a weak La Nina event fully expected by early winter. We detailed last week how, overall, South American yields tend to be capped in La Nina years, which at the least will keep the market on high alert for adversity in the weeks/months ahead.

Dryness looks to return to eastern Australia through the balance of the growing season, and while marginally better rainfall in mid-Oct was helpful, private Aussie wheat crop estimates remain at/below 20 MMTs, vs. the USDA’s 22.5. Aussie wheat replacement costs in New South Wales this week rest at $250-270/MT, vs. $160/MT in Russia and $220/MT in the US, basis HRW.

We view today’s action a mostly a function of fund short covering, with, again, the tail end of harvest at least on the horizon. Funds through last Tuesday expanded their net short positions modestly, but they’ve been further expanded since. ARC estimates funds’ net short in corn as of this AM at a lofty 185,000 contracts, vs. 70,000 contracts in late Oct a year ago. Funds have been short corn in excess of 200,000 contracts only briefly in the last two years.

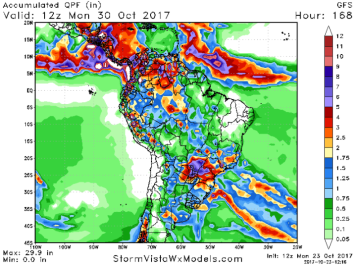

Midday GFS South American Weather Update: The midday GFS is wetter in Central & Northern Brazil, and drier elsewhere in South America next week. In the near term heavy rain will continue to plague planting efforts in key areas of Argentina’s crop belt, while only scattered showers are forecast in Mato Grosso, Goias and Minas Gerais into early next week. A shift to a more normal pattern of moisture is indicated in Brazil, but confidence in the details requires further model runs. 7-day precip is below.

AgResource Market Comment: A test of recent lows was warranted amid transportation issues but ARC cautions against turning bearish, however, until trend yields can be confirmed in S America in mid- to late winter.