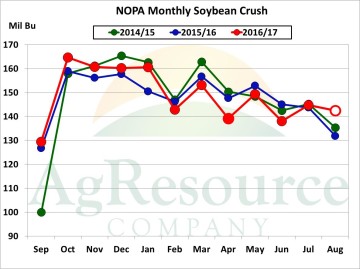

NOPA-member crush in August totaled 142.4 Mil Bu, down 2 Mil from July but a record for the month – and up a noticeable 5 Mil from the prior August record set in 2006! Assuming the normal Census/NOPA relationship, official US soybean crush in August is forecast at 153 Mil. Final 2016/17 soy crush is then pegged at 1,900 Mil Bu, 5 Mil higher than the USDA’s forecast this week. It’s not a meaningful change, but yet more beans will be stripped from the US balance sheet. Crush margins have been rising slowly and since late August, have climbed to $.90-1.00/Bu – a 15 month high. Forward margins are higher still, and expect series of record/near record crush rates to be published in the Sep-Nov quarter For US soybeans.

NOPA-member crush in August totaled 142.4 Mil Bu, down 2 Mil from July but a record for the month – and up a noticeable 5 Mil from the prior August record set in 2006! Assuming the normal Census/NOPA relationship, official US soybean crush in August is forecast at 153 Mil. Final 2016/17 soy crush is then pegged at 1,900 Mil Bu, 5 Mil higher than the USDA’s forecast this week. It’s not a meaningful change, but yet more beans will be stripped from the US balance sheet. Crush margins have been rising slowly and since late August, have climbed to $.90-1.00/Bu – a 15 month high. Forward margins are higher still, and expect series of record/near record crush rates to be published in the Sep-Nov quarter For US soybeans.

Soy oil stocks on Aug 31st totaled just 1.42 Bil Lbs, down 14% from a year ago, the lowest for the month since 2014.

And indeed there remains a bullish story for world vegoil prices. Malaysia’s palm oil market is up sharply this week, and even at $.348/Lb, soy oil’s premium is not out of line with history. Malaysian palm stocks/use is recovering, but remains a long ways from the days of overabundance in 2014 and much of 2015. And of course to meet the US RFS, additional soyoil for biodiesel production must be found. A heavier burden will be placed on US veg oil & animal fat supplies to meet the Gov’t mandated use.

And indeed there remains a bullish story for world vegoil prices. Malaysia’s palm oil market is up sharply this week, and even at $.348/Lb, soy oil’s premium is not out of line with history. Malaysian palm stocks/use is recovering, but remains a long ways from the days of overabundance in 2014 and much of 2015. And of course to meet the US RFS, additional soyoil for biodiesel production must be found. A heavier burden will be placed on US veg oil & animal fat supplies to meet the Gov’t mandated use.

ARC pegs Midwest biodiesel margins at a positive $.15/Gal, and US plants will be crushing for soyoil rather than meal.

ARC doubts highs in the bean oil market have been scored, and biodiesel demand along with lower than expected US crude inventories will offer support on breaks. And there’s a demand story in the soybean market.