** Reversing the trends of recent days, the grains (corn/wheat) have caught a bid with soybeans and soymeal weaker in moderate volume. Corn is once again bouncing off of $3.45 support as the market continues to build a base against ever rising open interest (likely new fund shorts). ARC estimates that funds are now short a record 235-240,000 contracts of corn. The soybean rallied sharply for several days, but an attempt to fill an open chart gap at $9.62 has occurred. Wheat futures appear to be caught in between the pull of corn and the push of soybeans this AM. ARC looks for a mixed close as the CBOT grain room struggles to uncover volume and direction.

** CBOT brokers report that funds have bought 5,500 contracts of corn and 2,800 contracts of wheat, while selling 4,300 contracts of soybeans. In soy products, funds have sold 2,700 contracts of meal and 2,100 soyoil.

** Iran has issued a new tender for 200,000 MTs of feed barley while Tunisia canceled a tender for wheat, barley and durum. FAS reported 130,000 MTs of US soybeans sold to an unknown destination.

** US fob Gulf soybeans were offered this AM at $374/MT against Brazil at $382/MT with no Argentine offers noted. US soybeans are $.22/Bu cheaper for February than Brazil. Brazilian March fob soybeans are offered at $379/MT against the US at $375.00. The spread narrows which based on some premium for the Brazilian crop could allow world demand to switch southward.

** US farmers indicate that they will look to plant more cotton, sorghum and barley based on current prices and the outlook for their future profitability. US cotton acres could rise by 800,000-1.0 Mil acres to 13.5 Mil acres, sorghum acres back to 6.3-6.6 Mil acres (up 600-700,000 acres), and barley to 3.1-3.3 Mil acres (up 500-700,000 acres). The point is that minor crop acres including cotton could expand by 1.9-2.4 Mil acres which will come out of corn/soybean seeding with total US cropped acres unlikely to expand. This may cause a 500,000 acre decline in 2018 US soybean acres and 1-1.5 Mil acre drop in corn. This compares to the November Baseline report forecasting 2018 US corn and soybean acres both expanding to 91.0 Mil acres.

** Cattle futures are soaring to near limit gains with that 108 head traded at the Fed Cattle Exchange at $119.75. Fund buying of CME futures is pushing cattle to sharp daily gains as key chart based resistance is breached.

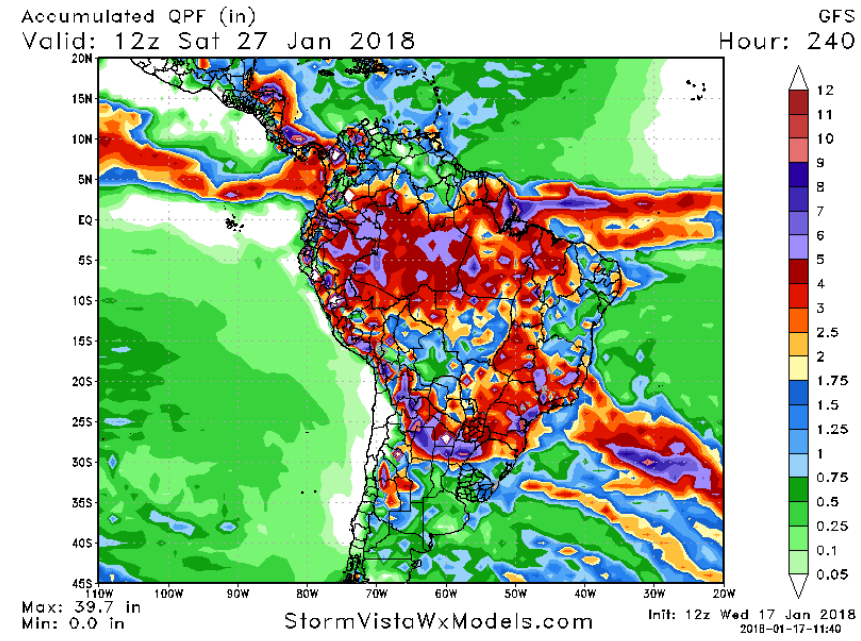

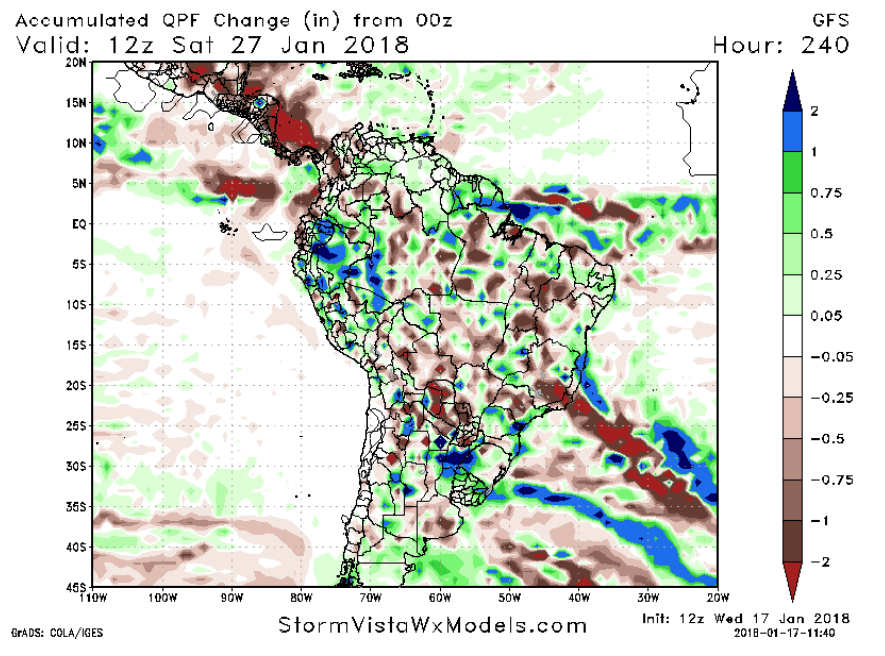

** Midday GFS South American Weather Forecast Discussion: The GFS forecast is little changed from the overnight model run and its still far wetter than the European model for the northern half of Brazil next week. The forecast models are similar in that Argentina will hold in a below normal and above normal temp profile into early February. Rainfall totals over the next 10 days looks to range from .2-.8” across Argentina with locally heavier amounts. Unfortunately, this rain is not enough to counter evaporative losses and soil moisture levels will be in decline. The midday GFS does return rain across N Brazil in the 11-15 day period with ongoing dry weather for Argentina.

** AgResource Market Comment: US corn futures are rising as traders ponder reduced 2018 US corn seedings and a tightening balance sheet assuming a trend yield of 173 BPA. Soybean futures are weaker on spreading against the grains and the retesting of support in March soyoil futures below $.325. Our bias is that soyoil values are near long term support with limited downside risk as demand for US biodiesel increases. Amid funds that are holding a record large net short grain position, we continue to advise caution in new sales.