** AM trade at the CBOT has been mixed with corn, soybeans and wheat futures trading either side of unchanged. Crude oil prices have pushed above $61/ barrel for the first time since June of 2015 with the CRB/CCI index testing its prior monthly high. The next upside price target for March WTI crude oil rests at $62.58 – the top set back in early May of 2015. If crude prices can rise above this resistance, the next upside objective is $75-80/barrel, a target that is being advertised by the investment firm Blackstone. Inflationary chatter continues to swirl around the CBOT and what it will mean for the grains? Some wonder if hedge fund managers are waiting for next week’s January WASDE report before piling in? Nearly everyone expects next week’s USDA final crop and WASDE report to be bearish for corn/soybeans, a surprise would be a neutral or positive result.

** CBOT brokers report that funds have sold 2,000 contracts of corn and 500 contracts of soybeans, while buying 1,200 contracts of wheat. Funds are also flat in soymeal, while buying 2,200 contracts of soyoil.

** The first fields of soybeans have been harvested in N Brazil. Producers in Rondonopolis, Mato Grosso report average soybean yields at 55 bags/HA, some 2 bags less than last year. The harvest will be slow to move southward based on latent planting dates.

** China is more aggressively starting to ask for fob soybean offers for February/March soybeans and some new demand is being consummated from the US. The Brazilians will be slow to offer new crop soybeans based on late seeding dates and the pipeline being extremely depleted of old crop supply.

** Yesterday’s NASS November Fats & Oil report confirmed soyoil yield well below prior years (and market expectations). The report offering a soyoil yield of 11.4#/Bu vs 11.8#/Bu last year. The USDA estimated the 2016/17 US soyoil yield of 11.64#/Bu in the final count. ARC research argues that this year’s WASDE soyoil yield is overstated by .2-.4#/Bu or some 390-775 Mil pounds of production. The lower oil yield comes at a time of elevated demand of biodiesel due to import tariffs. The US can make up the oil shortfall with a larger crush pace, but the point is that US soyoil has a bull story going forward that will likely offer support to nearby soyoil futures on any break to $.33. ARC’s upside longer term target remains $.40-.42.

** This week’s US export sales report will be delayed until Friday due to Monday’s New Year holiday. A slow sales pace is expected due to holiday reduced demand. US weekly soybean sales may not exceed 1.0 MMTs.

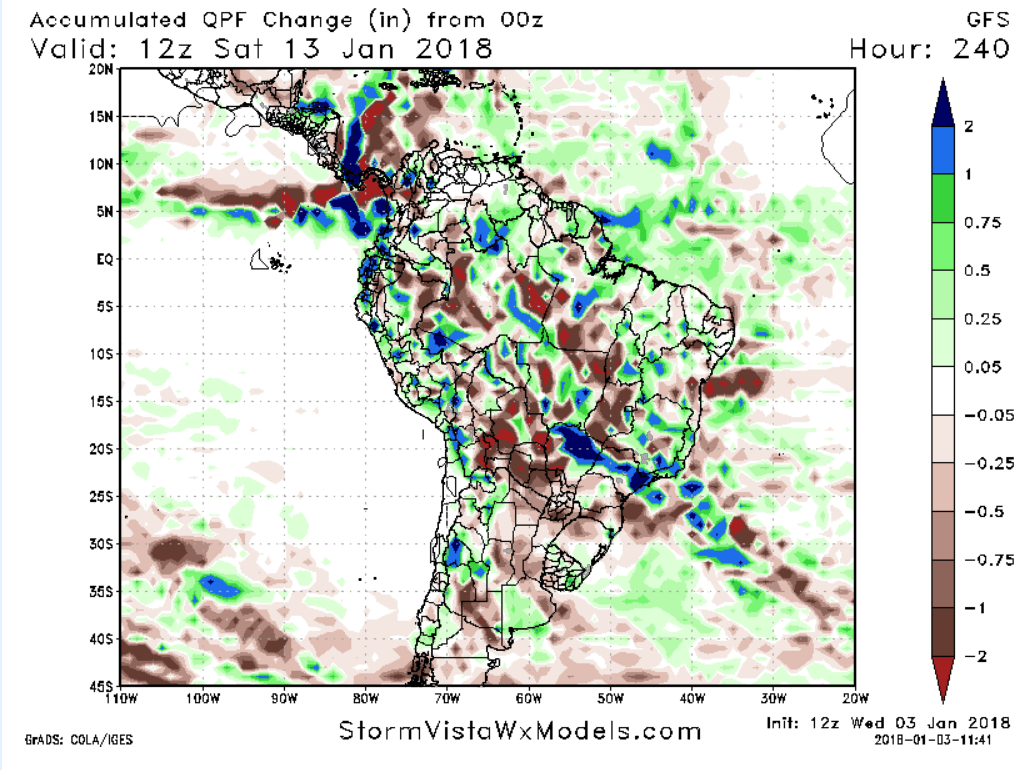

** Midday GFS Weather Forecast Discussion: The forecast is slightly drier than the overnight solution (which was dry already) for the next 10-11 days across Argentina and the southern third of Brazil. A late week warm front could produce a few spits of rain, but the overall forecast does not offer much rain with building heat for Argentina and S Brazil. High temps will warm to the 90’s and lower 100’s by Friday and persist into next week. The extended range 11-15 day offers some rain chances, but our confidence in the rain this far out is low. Our concern with Argy and S Brazilian weather is increasing.

Regular rains look to drop across the northern 2/3’s of Brazil with seasonal temps. Crops are preforming favorably amid a good mixture sunshine and moisture.

** AgResource Market Comment: There is a bull story developing in soyoil amid lower yield and sharp rise in biodiesel demand. Soyoil should gain on soymeal with normal Argentine weather. However, the forecast looks more concerning and drought issues are likely to emerge by mid January. ARC favors hard wheat gaining on soft in the weeks ahead on winterkill concern and historically low seeded acres. This is no time to be overly bearish corn, soy or wheat.