Larger than expected Northern Hemisphere (Russia namely) wheat crop size has been digested, and the market’s focus is shifting quickly to S Hemisphere prospects.

Larger than expected Northern Hemisphere (Russia namely) wheat crop size has been digested, and the market’s focus is shifting quickly to S Hemisphere prospects.

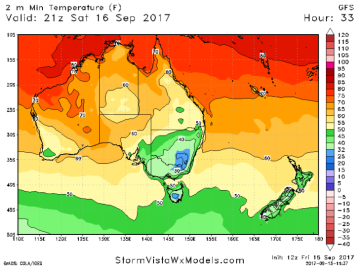

Australia will stay nearly completely dry into late month, and yet more frost scares is possible in NSW this weekend. The graphic below displays low temps in Australia late Sat. Freezing/near freezing lows will be widespread.

ARC maintains a neutral wheat outlook. Aussie and Argentine crops are being downgraded, but there’s just too much wheat in exportable positions currently, and until late 2017/early 2018, Russia will stay aggressive. Russian interior prices fell again this week, posting new 3-year lows. Southern Russia replacement costs are pegged at $155/MT, which is likely to keep Russian fob offers into October stable at $182-187/MT, basis spot. As such, for the US to stay competitive, KC/CME futures must trade in a range of $4.30-4.60, basis Dec.

Managed funds are short a net 84,000 contracts in Chicago, unchanged on the week, and lofty European prices will push demand to the US beyond fall. Stay patient and extend sales & hedges on sharp rallies to $4.70 December Chi.