Spring wheat futures led the way down today, as Stats Can added 3 MMTs to Canada’s all-wheat production total. This goes a long way in easing concerns over the availability of high protein wheat in North America, and also suggests the US can boost cross-border trade if any real shortages develop. ARC notes that Stats Can production figures are now largely satellite based, but any correction to production awaits Stats Can’s next stocks report, which isnt due until early February. Funds sold and estimated 4,500 contracts in Chicago.

Spring wheat futures led the way down today, as Stats Can added 3 MMTs to Canada’s all-wheat production total. This goes a long way in easing concerns over the availability of high protein wheat in North America, and also suggests the US can boost cross-border trade if any real shortages develop. ARC notes that Stats Can production figures are now largely satellite based, but any correction to production awaits Stats Can’s next stocks report, which isnt due until early February. Funds sold and estimated 4,500 contracts in Chicago.

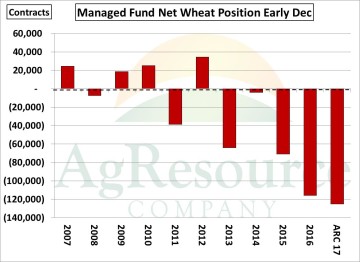

World markets also ended lower following Stats Can’s report, with EU origin wheat down a full $3-4/MT this evening, but the news should be fully digested by early Thursday. Otherwise, US export sales are likely to rise slowly as, on paper, the Gulf HRW market is more competitive. Managed funds’ net short today is calculated at 125,000 contracts, which is sizeable. ARC looks for a modest rebound from contract lows, but does note that rallies require the loss of corn yield in South America.