Relative to trade estimates, the January Cattle report did not offer any major surprises. Changes to last year’s inventory totals were minimal, and the 2018 inventory numbers were generally as expected, but total cattle and calves were confirmed at a 9 year high of 94.4 Mil head. The January 1st beef cow number rose by 510,000 head (1.6%) from a year ago, as cow/calf margins in 2017 rebounded from losses in 2016. As seen in the char this the 4th consecutive year of beef cow herd expansion, which has not occurred since the early 1990’s. By state, SD added 137,000 beef cows (+8%), TX increased it’s herd by 125,000 head (+3%), and MO added 111,000 head (+5%). In the major cow/calf states, KS cut their herd by 63,000 head (4%), and the NE herd was down 10,000 (1%).

Relative to trade estimates, the January Cattle report did not offer any major surprises. Changes to last year’s inventory totals were minimal, and the 2018 inventory numbers were generally as expected, but total cattle and calves were confirmed at a 9 year high of 94.4 Mil head. The January 1st beef cow number rose by 510,000 head (1.6%) from a year ago, as cow/calf margins in 2017 rebounded from losses in 2016. As seen in the char this the 4th consecutive year of beef cow herd expansion, which has not occurred since the early 1990’s. By state, SD added 137,000 beef cows (+8%), TX increased it’s herd by 125,000 head (+3%), and MO added 111,000 head (+5%). In the major cow/calf states, KS cut their herd by 63,000 head (4%), and the NE herd was down 10,000 (1%).

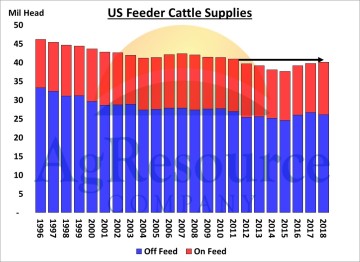

Total feeder cattle supplies (both on and off feed) as of January 1 were up 1% from a year ago, the largest since 2011 at 40.1 Mil head. Total steers and heifers on feed jumped 7% from last year to 6 year high of 14 Mil head, while feeder cattle supplies outside feedlots declined for the first time in 3 years – due to the large autumn placement rate (Plains drought) and totaled 26.1 Mil head. The tighter feeder cattle supply is viewed as supportive for the feeder cattle, but 2018 prices are expected to be similar to a year ago. The USDA’s January annual average feeder steer price forecast for 2018 was at $140-148, versus $145 in 2017, and $143 in 2016. The only unknown is whether a growing US economy leads to continued US red meat demand? The US will will have 10% more beef to consume this summer which is expected to push cash cattle prices below $100.00 for seasonal lows in June.