CBOT markets are higher at midday, driven by a more favorable macro landscape (crude is up $.30, the DOW up 300), and ongoing weather concerns in both hemispheres. There’s a better understanding by the trade that proposed tariffs from both the US & China won’t be implemented for some time. The GFS overnight trended cooler, and the midday so far maintains a lack of needed warmth across the N Plains & bulk of the Midwest. And some 95% of the Upper Midwest is blanketed by several inches of snow, which is unusual on this date. Soil temps in IA, MN & the Dakotas rest in the 20s & low 30s; a year ago soil temps there were in the 40s & 50s.

This week’s US Drought Monitor also showed a slight expansion in exceptional drought conditions across OK & CO, and still little to no rain is offered to the Western Plains into April 20th. HRW yield concern has been well documented, but ARC reminds clients that producers in TX, KS, OK and CO intend to plant just over 9 Mil Acres (11% of total) of corn there in 2018, as well as 5.6 Mil Acres soybeans.

Old & new crop US wheat export sales were disappointing at just 4 and 7 Mil Bu, respectively. Sales of other ag production were in line with to above trade guesses, and world soy complex demand does appear to be shifting to the US and away from South America.

Corn sales through the week ending last Thursday totaled 35 Mil, down from the prior week but still some 15 Mil above the pace needed to meet the USDA’s target. Total corn export commitments stand at 1,865 Mil, or a near record 84% of the USDA’s forecast. A 50-75 Mil Bu hike in US corn exports is nearly certain. Bean sales through the week totaled 42 Mil Bu, a record for this particular week (sales in late March typically range from 5-20 Mil). Total US bean commitments are now much better in line with the USDA’s forecast, and so perhaps no downward revision will occur in next Tuesday’s WASDE? Meal sales were a 9-week high 414,000 MTs, and meal commitments also rest a near record high 81% of the USDA’s forecast – with half the crop year remaining.

World wheat prices continue to move upwards, albeit slowly. An ongoing rail workers’ strike in France has pushed fob offers in France & Germany to new seasonal highs at $210-220/MT, still well below Gulf HRW offers but fundamental support is being raised to $4.80-4.90, basis July KC.

S America’s forecast remains much drier than normal across the southern half of Brazil’s safrinha corn belt through late Apr. It’s not too concerning at present, but whether the wet season has ended there needs close watching.

There’s still a few weeks before the bulk of Brazil’s 2nd corn crop begins pollinating, and a boost in soil moisture is needed in Mato Grosso do Sul & Parana, which typically produce some 45% of Brazil’s total safrinha crop.

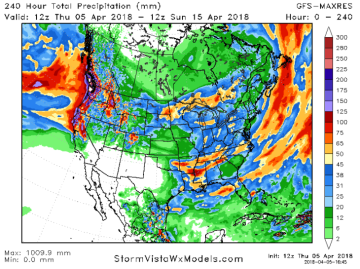

Midday GFS Weather Model Update: The midday GFS is little changed from the morning run. A few brief periods of warmer temps will occur across the Midwest beyond the next 6-7 days, but a needed lasting period of seasonal temps is not included into April 20th. Several more rounds of lite/moderate snow are offered to the Dakotas, MN, WI and IA over the next 10 days. Moderate rain is also forecast every few days in areas east of the MS River into late month.

AgResource Market Comment: Attention has shifted from global trade issues to less than ideal weather in the US & Brazil – and more rain is needed in Argentina and Australia over the next 30 days ahead of wheat planting. A choppy marketplace will persist, and we maintain sales should only be made on strong rallies.