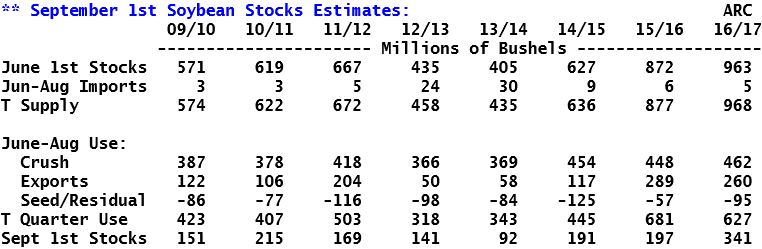

The USDA’s stocks estimates for the 2016/17 crop year have been in a wide range over the last year. The peak estimate was in December at 480 Mil Bu, with estimates steadily grinding lower to the most recent forecast of 345 Mil Bu. Crush estimates have moved lower over the last year, largely due to slower meal export. However, lower crush has been more than offset by rising exports. Residual was also lowered following the March stocks report, and in recent years, declining residual has preceded an increase in the crop size in the Sep stocks report. ARC estimates a 4th quarter residual of -95 Mil Bu, with Sep 1 stocks at 341 Mil Bu, assuming no change in the 2016/17 crop size.

The USDA’s stocks estimates for the 2016/17 crop year have been in a wide range over the last year. The peak estimate was in December at 480 Mil Bu, with estimates steadily grinding lower to the most recent forecast of 345 Mil Bu. Crush estimates have moved lower over the last year, largely due to slower meal export. However, lower crush has been more than offset by rising exports. Residual was also lowered following the March stocks report, and in recent years, declining residual has preceded an increase in the crop size in the Sep stocks report. ARC estimates a 4th quarter residual of -95 Mil Bu, with Sep 1 stocks at 341 Mil Bu, assuming no change in the 2016/17 crop size.

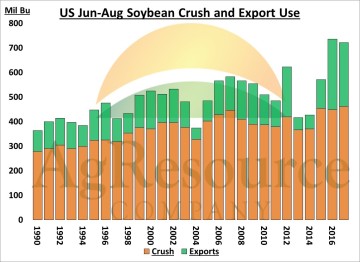

US soy crush and export use can be estimated fairly accurately based on weekly/monthly trade reports from the USDA – and the monthly crush data from NOPA. Total US quarterly exports are estimated at 260 Mil Bu, down slightly from a year ago as Brazil continued to export large quantities through the summer, but will still be the 2nd largest summer export rate on record.

US soy crush and export use can be estimated fairly accurately based on weekly/monthly trade reports from the USDA – and the monthly crush data from NOPA. Total US quarterly exports are estimated at 260 Mil Bu, down slightly from a year ago as Brazil continued to export large quantities through the summer, but will still be the 2nd largest summer export rate on record.

Soy crush spreads at the CBOT remained well above average through the summer, thought estimated margins in the cash market were lower on negative meal basis. Nevertheless, the quarterly crush rate is estimated just over 460 Mil Bu, and record large for the quarter.

Combined crush/export use is estimated to be down fractionally from a year ago at 722 Mil Bu, but will also be the 2nd largest quarterly usage rate on record.

With crush, and exports generally known, the final piece of the quarterly stocks calculation left to understand is the residual. The USDA lowered their estimate for annual residual to 14 Mil Bu following the March stocks report, which showed a larger than expected Dec-Feb residual total. The data hints that NASS may have underestimated the size of 2016/17 crop. Small revisions to acreage and yield can be expected in next week’s quarterly stocks report.

AgResource estimates Jun-Aug residual at -109 Mil Bu, which is near average with the last several years, and puts the annual residual total at 0.

Based on the preliminary crush and export data for August, we think annual the annual crush could be 10 Mil Bu more than the September WASDE while exports will be close to the USDA forecast. Assuming no change in the 2016/17 crop size, Sep 1 soybean stocks could be lowered 4 Mil Bu to 341 million – a non event for the market if US 2017 soybean yields are correct at 49.9 BPA?