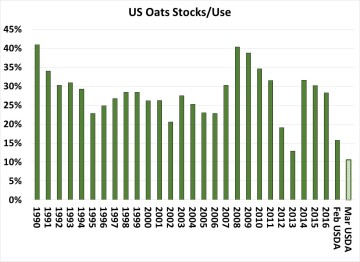

Somewhat quietly the USDA in its March WASDE lowered US oats ending stocks by 10 Mil Bu to a record low 20 Mil. Stocks/use, too, is now projected to record low in 17/18 as the market has not been able to slow consumption – despite sharply higher prices this year. Following Stats Canada’s stocks report in February, the USDA was forced to raise Canada’s domestic use, thus taking supply off the world market. Imports into the US from Canada were lowered 10 Mil Bu to 90 Mil Bu. This lack of supply was taken directly out of US end stocks. The USDA’s move last week further raises the need to expand oat seedings in the US & Canada this spring, and there’s simply no room for yield error in the North American oat balance sheet. It also remains that producers in the N Plains will opt to expand oats, barley & spring wheat acres at the cost of corn – and potentially soybeans.

Somewhat quietly the USDA in its March WASDE lowered US oats ending stocks by 10 Mil Bu to a record low 20 Mil. Stocks/use, too, is now projected to record low in 17/18 as the market has not been able to slow consumption – despite sharply higher prices this year. Following Stats Canada’s stocks report in February, the USDA was forced to raise Canada’s domestic use, thus taking supply off the world market. Imports into the US from Canada were lowered 10 Mil Bu to 90 Mil Bu. This lack of supply was taken directly out of US end stocks. The USDA’s move last week further raises the need to expand oat seedings in the US & Canada this spring, and there’s simply no room for yield error in the North American oat balance sheet. It also remains that producers in the N Plains will opt to expand oats, barley & spring wheat acres at the cost of corn – and potentially soybeans.

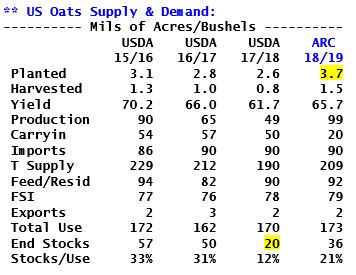

The oats market just after harvest rallied sharply to slow use and entice additional new crop acres. For context, US oats production in 17/18 totaled just 49 Mil Bu, down 16 Mil from the previous year and down 18 Mil from the USDA’s original balance sheet in last May’s WASDE. Cash oat prices were the cheapest feedgrain in the Plains last spring, and like in so many locations, this year it is the most expensive grain currently. Notice in the graphic at left that cash oats prices are nearing $180/MT, the highest price since the middle part of 2014. Despite the rally the USDA’s domestic consumption forecast has been unchanged all year. Expanded acres are required to keep end stocks at/above pipeline in 2018/19. Also notice that barley prices have been rising in recent weeks as the world barley stocks look to fall to a 34-year low in 2017/18.

The oats market just after harvest rallied sharply to slow use and entice additional new crop acres. For context, US oats production in 17/18 totaled just 49 Mil Bu, down 16 Mil from the previous year and down 18 Mil from the USDA’s original balance sheet in last May’s WASDE. Cash oat prices were the cheapest feedgrain in the Plains last spring, and like in so many locations, this year it is the most expensive grain currently. Notice in the graphic at left that cash oats prices are nearing $180/MT, the highest price since the middle part of 2014. Despite the rally the USDA’s domestic consumption forecast has been unchanged all year. Expanded acres are required to keep end stocks at/above pipeline in 2018/19. Also notice that barley prices have been rising in recent weeks as the world barley stocks look to fall to a 34-year low in 2017/18.

The USDA did not provide a new crop oats balance sheet at its Annual Outlook Forum in February, but our work suggests that a minimum of 3.7 Mil Acres (a 12-year high, and up a full Mil from last year) needs to be planted. Otherwise, the buffer against yield loss will be nonexistent and even seedings of 3.7 Mil won’t fully replenish US supplies to the levels of 2015 & 2016! Note that if US oat seeding intentions are below 3.0 Mil, new crop end stocks fall below 15 Mil Bu. WI, TX, SD, ND and MN account for a little over half of US oats planted acreage. ND, SD and MN also account for roughly 70% of US spring acreage – and that market also needs a expansion in area – and so outside of the primary ag belt, ARC fully expects corn area to be down from a year ago. We also advise end users to extend oats coverage on moderate breaks in the near term, and to target $2.30-2.40, Dec 18, to extend new crop coverage.

The USDA did not provide a new crop oats balance sheet at its Annual Outlook Forum in February, but our work suggests that a minimum of 3.7 Mil Acres (a 12-year high, and up a full Mil from last year) needs to be planted. Otherwise, the buffer against yield loss will be nonexistent and even seedings of 3.7 Mil won’t fully replenish US supplies to the levels of 2015 & 2016! Note that if US oat seeding intentions are below 3.0 Mil, new crop end stocks fall below 15 Mil Bu. WI, TX, SD, ND and MN account for a little over half of US oats planted acreage. ND, SD and MN also account for roughly 70% of US spring acreage – and that market also needs a expansion in area – and so outside of the primary ag belt, ARC fully expects corn area to be down from a year ago. We also advise end users to extend oats coverage on moderate breaks in the near term, and to target $2.30-2.40, Dec 18, to extend new crop coverage.