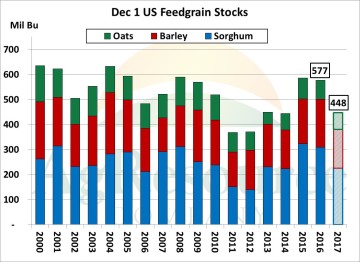

Non-corn US feedgrain stocks as of Dec 1st were revealed close to expectations, and aside from raising US sorghum yield & stocks very slightly the USDA made no changes to annual US balance sheets. Combined stocks on Dec 1st totaled 448 Mil Bu, down 129 Mil Bu (22%) from a year ago. Combined stocks/use of sorghum, barley and oats totaled 124%, vs. 138% last year, which suggests the market is tight but there’s no shortage of lesser followed feedgrain stocks in the near term. However, US imports surged in the first quarter of its marketing year, and sorghum disappearance is expected to accelerate as previously sold bushels are shipped in the next several weeks. Sorghum sales in mid-November have routinely exceeded the pace needed to meet the USDA’s target by 3-9 Mil Bu, or some 100-300%.

Non-corn US feedgrain stocks as of Dec 1st were revealed close to expectations, and aside from raising US sorghum yield & stocks very slightly the USDA made no changes to annual US balance sheets. Combined stocks on Dec 1st totaled 448 Mil Bu, down 129 Mil Bu (22%) from a year ago. Combined stocks/use of sorghum, barley and oats totaled 124%, vs. 138% last year, which suggests the market is tight but there’s no shortage of lesser followed feedgrain stocks in the near term. However, US imports surged in the first quarter of its marketing year, and sorghum disappearance is expected to accelerate as previously sold bushels are shipped in the next several weeks. Sorghum sales in mid-November have routinely exceeded the pace needed to meet the USDA’s target by 3-9 Mil Bu, or some 100-300%.

Non-corn feedgrain stocks in the US certainly are not adequate, and those markets in the next 60-90 days will work to keep domestic use slowed, oat imports enlarged, and to secure additional acreage next spring.

Non-corn feedgrain stocks in the US certainly are not adequate, and those markets in the next 60-90 days will work to keep domestic use slowed, oat imports enlarged, and to secure additional acreage next spring.

On balance, via higher sorghum yield, combined sorghum, barley and oat stocks in the US were raised 3 Mil Bu in the USDA’s Jan WASDE. World feedgrain stocks, however, were lowered slightly and it remains that combined global stocks and stocks/use of lesser followed feedgrains will be record low in 2017/18. Assuming trend yield and demand growth, unchanged global acreage will allow feedgrain stocks and stocks/use to fall further. The point is that additional global acreage is required to prevent untenable combined sorghum, oat & barley supply and demand.

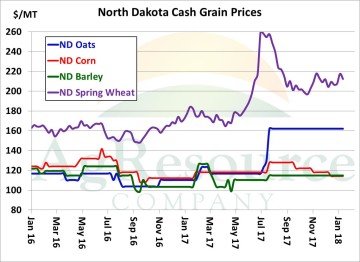

Non-corn grain prices (basis especially) have been rising steadily since the end of summer. And that this is a fundamental issue raises more uncertainty over soybean and – especially – corn acreage in fringe producing areas this spring. In Central ND, like in Central KS and other places, corn is now the cheapest grain, and thus incentive to maintain corn acreage across the Plains is rather low. Just this week cash barley prices are marginally higher than corn. Tightness in non-corn feedgrain supply & demand will keep prices elevated (sorghum’s outlook is most positive, as it’s a function of export demand), and thus work to curtail corn seedings across the Plains & Delta/Southeast. NASS’s Dec 1 stocks report was not minor feedgrains.

Non-corn grain prices (basis especially) have been rising steadily since the end of summer. And that this is a fundamental issue raises more uncertainty over soybean and – especially – corn acreage in fringe producing areas this spring. In Central ND, like in Central KS and other places, corn is now the cheapest grain, and thus incentive to maintain corn acreage across the Plains is rather low. Just this week cash barley prices are marginally higher than corn. Tightness in non-corn feedgrain supply & demand will keep prices elevated (sorghum’s outlook is most positive, as it’s a function of export demand), and thus work to curtail corn seedings across the Plains & Delta/Southeast. NASS’s Dec 1 stocks report was not minor feedgrains.