Commodity Index

The CCI/CRB Index closed higher on the week, but at the lower end of the range on late week profit taking. Energy prices eased on the moderation of arctic cold across the Central US, while the US dollar held in a narrow range.

The CCI/CRB Index closed higher on the week, but at the lower end of the range on late week profit taking. Energy prices eased on the moderation of arctic cold across the Central US, while the US dollar held in a narrow range.

The CRB confirmed a bullish trend last week and a test of support at 420.10 should produce the next buying opportunity.

A break below recent week lows would confirm a new leg down for the US greenback as the US budget deficit starts to rapidly expand in February with the installation of the Trump Tax program. The financial markets are struggling to understand the amount of US dollars that will be brought back from overseas?

The ongoing expansion of the US and world economic landscape will keep the CRB index heading upwards into mid 2018 when midterm election debate will commence.

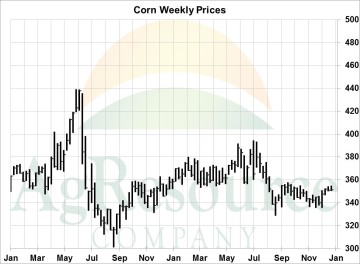

Corn

The corn market ended the week flat. Quarterly US stocks are expected to be revealed next week at a record large 12.4 Bil Bu, but at the same time US corn is the world’s cheapest feedgrain, and interior wheat & sorghum basis is firming. There’s still no compelling evidence to support a major bull or bear move in the near term. South American weather will remain critical.

ARC does note that the recovery since December’s expiration has been at least somewhat cash market-led, which is important, and with Argentina’s crop pollinating in rather stressful conditions downside risk into Feb/Mar is limited. Energy markets are well supported, and there’s enough uncertainty surrounding South America’s surplus in 2018 that we remain patient in extending sales. Don’t panic on breaks, though like in recent years any test of $4.00, Dec 18, should be rewarded. A major US drought would be needed to change the longer term sideways trading range in corn.

Wheat

Wheat futures rallied to modest gains, led by higher protein contracts in KC and Minneapolis, as funds covered part their massive net short position. Bitterly cold temps have also triggered uncertainly over HRW yield potential, but winterkill losses cannot be quantified until spring. And a quick moderation in temps is expected in the next 2 weeks with some moisture.

Otherwise, the graphic shows that spot CME futures have ranged between $4.00-4.50 for months. This range is fully expected to continue amid large surpluses globally.

We do advise against turning bearish on breaks, however, amid continued severe dryness across the US Plains, a complete lack of snow cover in Southern Russia, a weakening US dollar could allow for rallies come spring. Await a test of $4.80+ July CME, to extend new crop sales. Longer term, the price outlook hinges on Russian 2018 yields/production.

Soybeans

It was a mostly higher week of holiday shortened trade in the CBOT soy markets, that futures higher at Friday’s close. Concerns for S American weather and crops supported trade through the week on fund short covering. Fundamentally, the USDA is expected to report record large US Dec 1 soybean stocks next week, and at the same time the S American crops are far from being made. Early Brazilian harvest is just now getting udnerway and the lineup alread shows more than 1 MMTs to sail in January. However, there is still a large amount of the Argentine crop to be planted, and a large percentage of the growing crop that is in need of rain. Funds are holding the largest short soybean position since July while hedgers are net long, which looks to support the soybean market heading into the important USDA January reports. We await short covering rallies back to $10 or better for new sales.The trendline offers support post the USDA report.

Cattle

It was a mixed week of trade in the hog market, with nearby February under pressure from weaker cash prices, while summer hog futures all marked new contract highs. Supply fundamentals remain bearish, and the question going forward is whether demand will again increase to keep prices unchanged or higher from a year ago. The nearest level of technical resistance on the weekly nearby chart is at the top side of a chart gap near $80, that was left with the July expiration. However, note that in the last 2 years, the $80 level has not been traded until late spring, which we expect will hold true again this year.

Longer term, ARC research argues that strong rallies over $85 basis summer hog futures should be sold as record US red meat production offers downside price risk beyond April.