Commodity Index

The CCI/CRB index settled slightly lower on the week as it was disappointing that the index was unable poke above the prior week’s high. The technical base that the CRB has formed argues for a larger rally, but crude oil is going to have to push above $52/barrel with the metal markets sliding lower.

The US Central Bank confirmed a more hawkish view in their Sept 20th Meet amid their starting to unwind a $4 Trillion balance sheet. The long end of the interest rate market did not move much on sluggish inflation expectations, but the 10 year could reach 3% sometime in 2018.

The world economy continues to outperform and our view on commodity valuations remains positive. We are not willing to chase rallies, but would buy breaks. Our initial upside target is 420-421 by the 4th quarter.

Corn

Dec corn ended near unchanged, as the market continues to flirt with major resistance at $3.55. A flood of combine yield data in the next few weeks will drive nearby direction. So far yield data has been variable, and a clear yield trend is lacking; overall the debate over whether yield is 166-169 is ongoing. ARC doesn’t expect much of the corn market into mid-fall. Even a yield of 166 only barely changes the US balance sheet, and end stocks anywhere from 1.9-2.3 Bil Bu suggests fair value lies between $3.35-3.75 basis spot CBOT futures. South America continues to ship record amounts of corn abroad, and US weekly export sales will be rather ho-hum into early 2018. Longer term, trend/above trend yields must be confirmed before bearish sentiment returns, and so we remain patient with respect to farm marketing. It’s far too early to be concerned, but a developing La Nina and delayed soybean seeding in Brazil (which in turn may delays safrinha corn planting) are being watched. No new sales are advised below $3.70 Dec ’17. The ethanol margins are strong so US domestic use is record large.

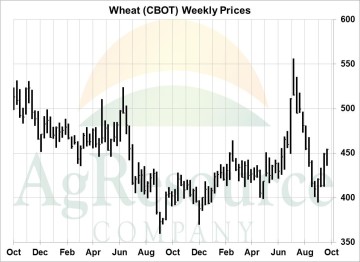

Wheat

Wheat futures rallied 1-14 cents with premium added to spring wheat values ahead of the Final US Small Grains Report next Friday. Fundamentally, it’s common for US/world wheat markets to bottom in late Aug/Sept, and with Russian fob offers rising rather quickly (as demand was found). A bearish outlook is not advised. Dec CME traded through major chart-based resistance on Thursday, and our work suggests Russian fob offers, a key driver of prices elsewhere, will test $194-196/MT basis spot, by Nov/Dec. This in turn allows the US market to be globally competitive in a range of $4.40-4.70 basis Dec CME/KC. As such, we continue to advise patience with respect to extending sales. We also note that Australia remains dry, Argentina has lost acreage, and a wetter pattern is needed in E Ukraine and S Russia for germination. Next resistance lies at $4.70 basis Dec CBOT where new sales will be advised.

Soybeans

Soybeans traded back and forth through much of the week with export demand offering support on early week selling. There were export sales announcements of nearly 1.7 MMTs of old crop soybeans for the week, while the weekly export sale report (prior week) showed sales last week that were well above expectations and the largest since last October at 2.3 MMTs. Domestic Chinese meal pricing ahead of next week’s holiday was also robust. The Midwest harvest is underway with highly variable results, but a trend that is below last year. ARC expects that by Sunday evening 11-14% of the US soybean crop will have been harvested/ The harvest in the Delta will pass 50%, while warm/dry weather in the has pushed Midwest seed dry down. November soybeans broke through several key layers of resistance in Friday’s trading, leaving the next key technical level at a trend line near $10. However, trading looks to slow by the middle of next week as the market prepares for the uncertainty of the Quarterly Stocks report out next Friday.

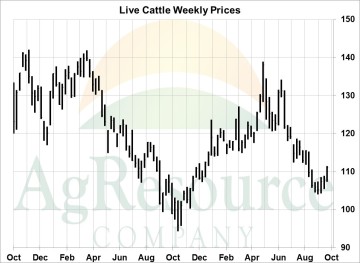

Cattle

Trading in the cattle markets was slow, but generally firm to start the week. A strong rally developed at midweek on ideas that this week’s cash cattle trade would be higher. December cattle marked the best gain for the week, pushing through several key technical levels on Wednesday at prices that haven’t been seen since mid-July. Fundamentally, the market is well supplied with carcass weights seasonally recovering while cattle kill rates are large. The September Slaughter Report confirmed US beef production during July at 106% of a year ago, and the market outlook into the end of the year still calls for record large beef production in the 4th quarter. This week’s rally is giving feedlots the chance for profitable 4th quarter sales. A top for early 2018 is forecast for the $123-128 price range.

Hogs

The hog m arket traded steady to higher early in the week, before turning sharply lower. October hogs slipped to new contract lows in Thursday and Friday’s trading, while an early week rally in December hogs was wiped out by late week selling. Weekly hog kills are now quickly expanding to new records, while hog carcass weights are now holding well above a year ago. Record large US pork production will keep the longer term hog and pork market outlook bearish. Next week’s Quarterly US Hog & Pigs report should confirm a record large summer pig crop, and is also expected to show expansion in fall farrowing intentions. Initial targets for spot futures are just $2-3 lower, though December hogs are still trading nearly $14 above last year’s seasonal bottom. Pork belly stocks remain historically tight, and if demand remains as strong as a year ago, that could lift their seasonal lows by $5-7.

arket traded steady to higher early in the week, before turning sharply lower. October hogs slipped to new contract lows in Thursday and Friday’s trading, while an early week rally in December hogs was wiped out by late week selling. Weekly hog kills are now quickly expanding to new records, while hog carcass weights are now holding well above a year ago. Record large US pork production will keep the longer term hog and pork market outlook bearish. Next week’s Quarterly US Hog & Pigs report should confirm a record large summer pig crop, and is also expected to show expansion in fall farrowing intentions. Initial targets for spot futures are just $2-3 lower, though December hogs are still trading nearly $14 above last year’s seasonal bottom. Pork belly stocks remain historically tight, and if demand remains as strong as a year ago, that could lift their seasonal lows by $5-7.