Commodity Index

The CCI/CRB index held in a tight range and closed slightly lower at 406.20. Since early August, the CRB has not been able to garner much upside potential, but rising energy prices has helped underpin the index on breaks. And, the US dollar closed higher on the Trump Tax Proposal, but it’s now the speed of any future legislation which will be directing the greenback. ARC notes that the odds are 70% that the FED will be raising their interest rates in December.

ARC looks for another two US Central Bank rate increases in 2018. The short end of the interest rate curve is rising, while anyone that borrows longer than 10 years is seeing rates below the levels at the same time last year.

ARC’s research maintains a modestly bullish outlook on the CRB for a further bump higher into late 2017. The export pace of emerging markets looks to be supportive to further CRB gains.

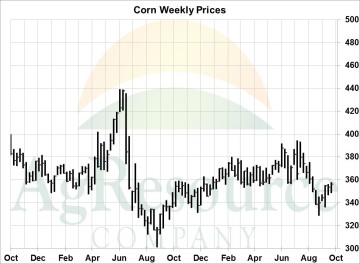

Corn

December ended the week 2 cents higher, driven in large part by a modestly supportive Sep 1 stocks report. Final 16/17 US corn end stocks were pegged at 2,295 Mil Bu, down 55 Mil from trade guesses, which will act to marginally tighten old and new crop balance sheets (assuming the US yield is unchanged). ARC maintains a national yield forecast of 166 Bu/Acre, which if realized will pull new crop end stocks closer to 2.00 Bil Bu. Otherwise, fresh news is lacking, but ARC does mention that other feedgrain costs are rising, and in some cases rather sharply. Black Sea feed wheat is now offered a full $20/MT above Gulf corn, and world barley prices hit multi-year highs. Seasonal trends in wheat point higher through late year and corn is expected to follow to some extent. Target $3.75+, basis Dec, to catch up on sales, and we strongly urge producer clients to hedge a portion of the ’18 crop at $4.00+ basis Dec 18 futures. Corn looks to be range bound.

Wheat

US futures ended lower, led by spring wheat in Minneapolis amid a larger than expected final crop estimate from NASS. Spring wheat’s premium to other classes will erode as a result, but overall ARC expects the US wheat market to shrug off this week’s bearish data pretty quickly. Black Sea & European markets continue to move higher, severe dryness shows no signs of ending in New South Wales in Australia, and funds in Chicago maintain a fairly sizeable net short position (65,000 contracts as of Tuesday). Lower protein Gulf HRW is now rather competitive in the world market, and recall the seasonal trend in Russian prices is noticeably bullish into Nov/Dec. Even Russia’s interior market is now moving higher despite record stocks there. Eventually, demand for high quality milling wheat will find the US, as Australian shipments will struggle beyond the next 30 days, and as winter plagues logistics in the Black Sea during winter. A range of $4.20-4.80 Dec CME is projected.

Soybeans

It was a mixed week of trade in the soybean market, futures were lower for the week, but well above the lows following the quarter Grain Stocks report. Soybeans traded down through most of the week ahead of the stocks report, but rallied following the report release as NASS slightly lowered their estimate of the 2016/17 soybean crop. This put the September 1 inventory well nearly 40 Mil Bu under expectations and supported trade in the final hours of the week. The trade now looks forward to the October Crop Report for guidance on yield and crop size. We note that with the smaller carry in, that it only takes a soybean yield of 48 BPA to pull US stocks under 250 Mil Bu. Chinese demand remains robust, and we expect that price breaks through harvest will find strong demand, while rallies back above $10.25 offer the new sales opportunity. Harvest lows are already in place, and support is offered below $9.40 November.

Cattle

The cattle market started the week with limit losses following the September Cattle on Feed report that showed a larger than expected August placement rate, and September 1st cattle on feed supplies that were at 104% of a year ago, the largest in 5 years. December cattle traded down through Tuesday, but found support from a strong early rally in beef prices, and then started to recover losses in the last half of the week on ideas that this week’s cash trade could be no worse than steady. And initial cattle sales for the week were near steady as cattle began trading at $107-108 on Thursday. December cattle finished the week lower, but were near the highs of the week. The outlook calls for record large beef production into the end of the year, which keeps the price outlook bearish on rallies. The US will have to chew through record large red meat supplies.

Hogs

Ho g futures started the week lower and then rallied to solid gains ahead of the hog inventory report. The report did not offer any surprises, but did confirm a record large summer pig crop and September 1 hog inventory that had been expected. The initial market reaction was a lower Friday open, which found strong demand that lifted hog futures to good gains on Friday. The cash hog market continues to move lower, on big kill rates and quickly rising carcass weights. Last week’s hog slaughter was a record weekly kill for September, and the 2nd largest 1 week kill total on record. The inventory report confirmed that 4th quarter pork production will be record large, with cash prices to fall at least another $5 to $10. December hogs continue to offer sales opportunities with any $2-3.00 rally.

g futures started the week lower and then rallied to solid gains ahead of the hog inventory report. The report did not offer any surprises, but did confirm a record large summer pig crop and September 1 hog inventory that had been expected. The initial market reaction was a lower Friday open, which found strong demand that lifted hog futures to good gains on Friday. The cash hog market continues to move lower, on big kill rates and quickly rising carcass weights. Last week’s hog slaughter was a record weekly kill for September, and the 2nd largest 1 week kill total on record. The inventory report confirmed that 4th quarter pork production will be record large, with cash prices to fall at least another $5 to $10. December hogs continue to offer sales opportunities with any $2-3.00 rally.