Commodity Index

The CCI this week ended with very slight gains, with is noteworthy in the face of a rising US dollar and renewed concern over emerging economies – at least currencies there. Somewhat quietly, currencies in Australia, Canada, Brazil and Argentina have weakened noticeably since early October, and in some cases are now down on the year. This is hurting US grain export potential in the short run, as after being somewhat cheap US wheat is now priced at a premium to comparable EU & Black Sea origin. Argentine corn, too, is still very cheap. But, ARC contacts suggest economic growth is occurring in South America, albeit slowly, and so we doubt currency weakness will be a lasting phenomenon. US crude supplies remain below last year, and gasoline stocks are fairly tight. Strength in crude will be additionally supportive to emerging market growth longer term.

The CCI this week ended with very slight gains, with is noteworthy in the face of a rising US dollar and renewed concern over emerging economies – at least currencies there. Somewhat quietly, currencies in Australia, Canada, Brazil and Argentina have weakened noticeably since early October, and in some cases are now down on the year. This is hurting US grain export potential in the short run, as after being somewhat cheap US wheat is now priced at a premium to comparable EU & Black Sea origin. Argentine corn, too, is still very cheap. But, ARC contacts suggest economic growth is occurring in South America, albeit slowly, and so we doubt currency weakness will be a lasting phenomenon. US crude supplies remain below last year, and gasoline stocks are fairly tight. Strength in crude will be additionally supportive to emerging market growth longer term.

Corn

Dec corn ended just modestly higher, which so far likely confirms that a secondary seasonal bottom was scored last week. But otherwise the market looks bound to a range of $3.45-3.55 into early winter, with South American climate forecasts to drive value thereafter. ARC maintains a strategy of buying breaks, but also selling even slight rallies, and we advise against turning too bearish on weakness. Ethanol production remains rather impressive in spite of falling margins. US export sales have exceeded expectation substantially in each of the last three weeks. And we detailed last week the negative correlation between La Nina and South American corn yields – and the arrival of weak La Nina is imminent.

Dec corn ended just modestly higher, which so far likely confirms that a secondary seasonal bottom was scored last week. But otherwise the market looks bound to a range of $3.45-3.55 into early winter, with South American climate forecasts to drive value thereafter. ARC maintains a strategy of buying breaks, but also selling even slight rallies, and we advise against turning too bearish on weakness. Ethanol production remains rather impressive in spite of falling margins. US export sales have exceeded expectation substantially in each of the last three weeks. And we detailed last week the negative correlation between La Nina and South American corn yields – and the arrival of weak La Nina is imminent.

Longer term, key will of course be Brazilian weather in Mar-May, but there are also questions surrounding N Hemisphere acreage amid another year of depressed margins in the US and reduced incentive to expand area worldwide. Only sell on rallies.

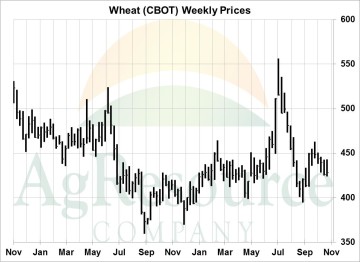

Wheat

US wheat futures ended slightly higher, but gave back much of the week’s gains amid declining currency values in a host of major exporting countries. This lowers the burden on exporters outside of the US to find incremental demand, and as such export sales through last Thursday were a bit below expectations – and slightly below the pace needed to hit the USDA’s forecast. And weather is mixed. Problems abound in the Southern Hemisphere, where too much rain has fallen in Southern Brazil and parts of Argentina, and where ARC’s contacts suggests spotty rainfall in early/mid-Oct did little to help the Aussie crop. Black Sea weather and US weather, however, is favorable. A longer term monthly uptrend line rests at $4.20, basis Dec CME, and we fully expect this to hold. Note that there’s talk of deep acreage cuts across the Central Plains, and US export potential should be boosted beginning in Dec/Jan, as Russia slows down. Await rallies to extend sales.

US wheat futures ended slightly higher, but gave back much of the week’s gains amid declining currency values in a host of major exporting countries. This lowers the burden on exporters outside of the US to find incremental demand, and as such export sales through last Thursday were a bit below expectations – and slightly below the pace needed to hit the USDA’s forecast. And weather is mixed. Problems abound in the Southern Hemisphere, where too much rain has fallen in Southern Brazil and parts of Argentina, and where ARC’s contacts suggests spotty rainfall in early/mid-Oct did little to help the Aussie crop. Black Sea weather and US weather, however, is favorable. A longer term monthly uptrend line rests at $4.20, basis Dec CME, and we fully expect this to hold. Note that there’s talk of deep acreage cuts across the Central Plains, and US export potential should be boosted beginning in Dec/Jan, as Russia slows down. Await rallies to extend sales.

Soybeans

November soybeans fell 7 cents – though traded in a very narrow range – as the pace of export sales & shipments falls further behind last year, and as finally a more normal pattern of rainfall develops in Central Brazil. Like grains, the outlook into early winter is neutral, and whether South American surpluses rise or fall in early/mid-2018 will determine whether the market breaks out of the long-established trading range. ARC does mention that, amid sluggish planting in Argentina, there’s a risk that acreage is shifted from beans to later planted corn, and already private analysts peg the Argi crop slightly below the USDA’s estimate. Rainfall in Jan/Feb will determine Brazil’s crop. And in the meantime, ARC suspects major importers are simply more hand to mouth this year – supplies are abundant, and there’s just not much incentive to extend coverage – and so the pace of US bean sales will stay elevated for some time. Continue to target $10+, basis March, to catch up on old crop pricing.

November soybeans fell 7 cents – though traded in a very narrow range – as the pace of export sales & shipments falls further behind last year, and as finally a more normal pattern of rainfall develops in Central Brazil. Like grains, the outlook into early winter is neutral, and whether South American surpluses rise or fall in early/mid-2018 will determine whether the market breaks out of the long-established trading range. ARC does mention that, amid sluggish planting in Argentina, there’s a risk that acreage is shifted from beans to later planted corn, and already private analysts peg the Argi crop slightly below the USDA’s estimate. Rainfall in Jan/Feb will determine Brazil’s crop. And in the meantime, ARC suspects major importers are simply more hand to mouth this year – supplies are abundant, and there’s just not much incentive to extend coverage – and so the pace of US bean sales will stay elevated for some time. Continue to target $10+, basis March, to catch up on old crop pricing.

Cattle

Cattle futures ended higher amid stable beef markets and amid abnormally cold temps – and some snow cover in the Northern Plains. Last week’s on-feed report was quickly shrugged off, and otherwise there’s just not enough bearish fodder yet to trigger any largescale fund liquidation. Seasonally, there’s still some upside risk in cash meat prices, and weekly slaughter likely peaked in mid-October.

Cattle futures ended higher amid stable beef markets and amid abnormally cold temps – and some snow cover in the Northern Plains. Last week’s on-feed report was quickly shrugged off, and otherwise there’s just not enough bearish fodder yet to trigger any largescale fund liquidation. Seasonally, there’s still some upside risk in cash meat prices, and weekly slaughter likely peaked in mid-October.

However, spot and deferred contracts are now touching our initial upside targets, and we advise new sales & hedges on any further strength. Above $127, our work suggest that Feb cattle have fully digested the forthcoming marginal slowdown in beef consumption, and the winter climate outlook for much of the Plains and Southern Midwest still lacks any lasting cold period. Funds this evening are estimated to be net long 110,000 contracts, which given current fundamentals appears excessive. It’s time to reward the recent advance.

Hogs

Hog futures ended near unchanged on the week, but also performed better than expected. Pork margins are slipping, but remain elevated, and key will be the price of pork into the holiday season. There’s no shortage of animal/meat supplies, but like a year ago a decent rally in belly prices is anticipated over the next 3-4 weeks. Until there are signs of a product-wide break in price, managed funds – which maintain a rather large net long position – will be reluctant to give in, and so we expect breaks to be supported, and least in the near term.

Hog futures ended near unchanged on the week, but also performed better than expected. Pork margins are slipping, but remain elevated, and key will be the price of pork into the holiday season. There’s no shortage of animal/meat supplies, but like a year ago a decent rally in belly prices is anticipated over the next 3-4 weeks. Until there are signs of a product-wide break in price, managed funds – which maintain a rather large net long position – will be reluctant to give in, and so we expect breaks to be supported, and least in the near term.

Longer term, ARC’s initial upside targets are being neared, and we’d look to use any further strength into mid/late November to boost sales and hedges. Red meat will be well supplied over the next several months, and while strength makes sense, we’d be careful being too bullish.