AgResource’s research suggests India will be a noticeable net wheat importer in 2018/19, even amid trend yields there. Indian wheat production has failed to meet domestic use for the last three years amid sizeable growth in food use. Even in 2017/18, in spite of record production, Indian wheat end stocks fell slightly and are currently projected at a 10-year low 9.7 MMTs.

AgResource’s research suggests India will be a noticeable net wheat importer in 2018/19, even amid trend yields there. Indian wheat production has failed to meet domestic use for the last three years amid sizeable growth in food use. Even in 2017/18, in spite of record production, Indian wheat end stocks fell slightly and are currently projected at a 10-year low 9.7 MMTs.

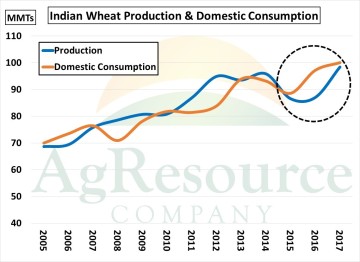

India has surpassed China in terms of annual GDP growth (India’s GDP is projected to grow by 7.7% into 2020, vs. Chinese growth of 6.3%, and world GDP growth of 3%), and is the next real driver of the world economy. Since 2015, Indian wheat food use has risen to 95 MMTs, up 13%, and which now nearly matches India’s annual wheat production potential. Total domestic wheat use, including feed, can be expected at 102-105 MMTs in the next few years, which requires new record seedings to prevent further stocks loss or elevated imports.

While wheat prices virtually worldwide have fallen in recent years, Indian milling quality cash prices are little changed – and thus Indian wheat is priced at a noticeable premium to the world, even including Australia. Since 2013, CME futures have lost 40% as world & major exporter stocks were built. Indian prices, however, are down only 10% at $268/MT, and in the last year have rallied $20/MT. Indian cash prices are in line with India’s relatively tight wheat balance sheet, and without a larger than expected expansion in seedings, it’s likely that India shifts to becoming a net wheat importer for the next several years. For context, in 2017 – again, despite record production – India will be a net importer of 1.5 MMTs of wheat. India was a net wheat exporter from 2012 to 2015.

While wheat prices virtually worldwide have fallen in recent years, Indian milling quality cash prices are little changed – and thus Indian wheat is priced at a noticeable premium to the world, even including Australia. Since 2013, CME futures have lost 40% as world & major exporter stocks were built. Indian prices, however, are down only 10% at $268/MT, and in the last year have rallied $20/MT. Indian cash prices are in line with India’s relatively tight wheat balance sheet, and without a larger than expected expansion in seedings, it’s likely that India shifts to becoming a net wheat importer for the next several years. For context, in 2017 – again, despite record production – India will be a net importer of 1.5 MMTs of wheat. India was a net wheat exporter from 2012 to 2015.

India’s monsoon last year, which is used for wheat irrigation, performed worse than expected. There’s also been talk of winter stress there in recent months. However, even amid trend yield Indian wheat consumption will continue to outpace production. India’s wheat balance sheet is attached, and ARC’s 2018 forecast assumes record area, trend yield and trends in domestic consumption. To keep stocks/use steady in 2018, imports of 5.3 MMTs are demanded. Thereafter, it’s possible that India imports some 5-6 MMTs in 2020.

India’s monsoon last year, which is used for wheat irrigation, performed worse than expected. There’s also been talk of winter stress there in recent months. However, even amid trend yield Indian wheat consumption will continue to outpace production. India’s wheat balance sheet is attached, and ARC’s 2018 forecast assumes record area, trend yield and trends in domestic consumption. To keep stocks/use steady in 2018, imports of 5.3 MMTs are demanded. Thereafter, it’s possible that India imports some 5-6 MMTs in 2020.

There’s still no shortage of wheat in exportable positions, but amid an expanding Central US drought, a tight balance sheet in Australia, a heavier burden is being placed on Black Sea yields this summer. All told, our work continues to suggest that breaks are opportunities to extend flour coverage.