** In keeping with the trend of recent trading days, CBOT corn, soybean and wheat futures are firmer, reversing prior day losses. The bears have been out in force following the September USDA crop report, but the market has not changed all that much on the week? The bears and bulls both are trying to decide on US corn/soybean yield trends, a debate that early harvest data has not solved. US corn yields are variable, but better than expected according to producers. Soybean yields have fared worse, but there is just not enough data to determine how far below the September NASS report could yields fall? Thus, the debate over yields is ongoing and it will take another week to 10 days of harvest data before clear yield trends evolve.

Key for the market is whether November soybeans can close above the 200 day moving average at $9.795? The market has run up against this resistance several times without breaking through. Selling pressure is noted above $9.75 November. A close above $9.80 November would turn chart trends upwards.

The same can be said about Dec Chi wheat above $3.50. Corn appears to be a follower until the cash industry sees that fund managers have had their fill on net short positions. ARC notes that option volatility is at a record low for late September which argues for grain market complacency. The low option vol means that if you a bull or a bear, calls or puts are a better purchase.

** The USDA reported new US soybean sales of 1.080 MMTs sold to an unknown destination with 132,000 MTs to China. The 1.080 MMTs of sales included 120,000 MTs of soybean sales for the 2018/19 crop year. The sales were a surprise,. It has some discussing whether framed contracts where held off shore and then brought to the US? We are told that China is getting ready for a week long holiday and active domestic meal sales sparked new US buying.

** The US weekly ethanol grind produced 303.7 Mil gallons vs 307.8 Mil gallons of ethanol last week. This production is well above last year and argues for a larger US annual US ethanol grind for 2017/18 based on hugely profitable margins. US ethanol stocks for the week were 888 Mil gallons, unchanged from last week, but up 6% from last year. US crude oil inventories were 473 Mil barrels, virtually unchanged from last year.

** China has placed 103 Mil HA or farmland (255 Mil acres) under permanent protection as theses acres should not be developed or used for non food production purposes. The move reflects China’s desire to protect productivity.

** Russia and the rest of the Black Sea is concentrating exporting high priced milling wheat, not feed wheat. This is why world feed wheat prices are rising which should bode favorably for October forward world corn exports. US fob corn is comparable to Brazilian offers, with Argentine corn far cheaper and being the most competitive in the world. South American corn exports should be record large for September as world feed grain trade/demand expands.

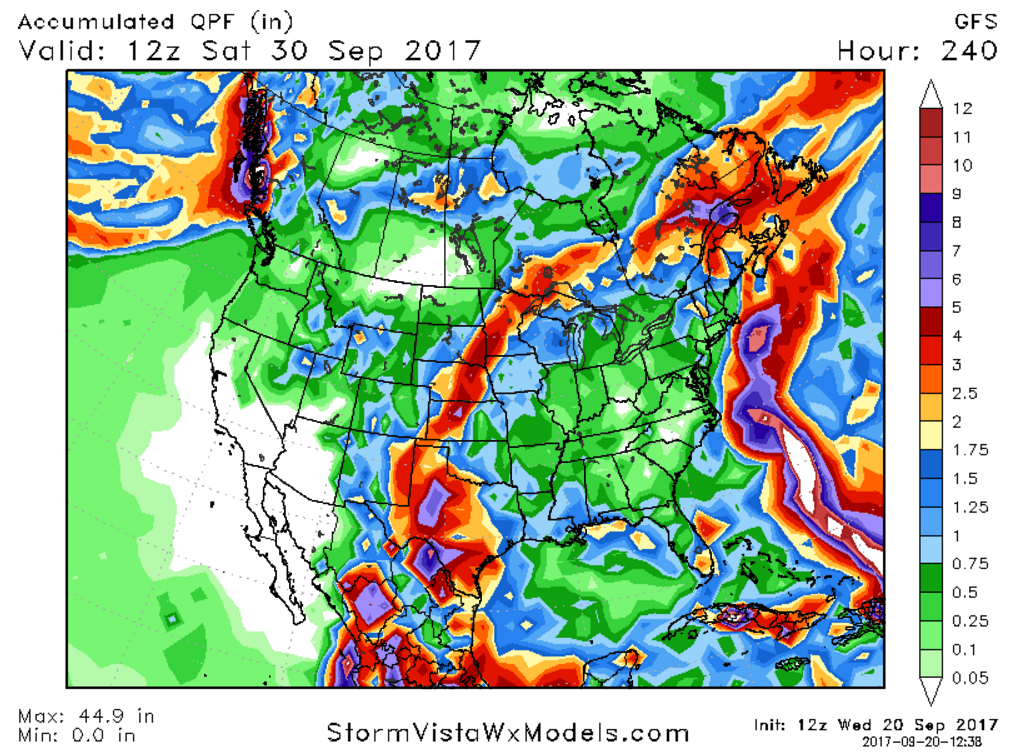

** Midday GFS Weather Model Forecast Update: The forecast is little changed from the overnight run with moderate to heavy rains slated to drop across the NW Midwest and the W Plains from a stuck Ridge/Trough pattern. 1-4.50” of rain looks to fall across; MN, NE, KS and TX over the next 6-8 days. The dry E Midwest will continue to see limited rainfall with active harvest expected to develop next week. Rain potential for the E Midwest looks to range from .1-.6” into the end of the month. Hurricane Maria looks to hug the US Eastern Shoreline, but not make landfall. High surf and wind looks to be featured across the far NE US. Temps average much above normal with highs in the 80’s to mid 90’s for the E Midwest. Some record highs are likely this weekend. The heat/dryness is pushing maturity.

** AgResource Market Comment: Follow through has been lacking in recent days at the CBOT as the “guts” of the ‘17 Midwest harvest looming and the Sept NASS yield debated. Funds/traders are lined up on the bear side of the market with farmers generally bullish. Two major USDA crop reports loom. Several large investment banks are again touting owning “hard assets” on breaks. The US Fed is out before the CBOT close.

** GFS Midday 10 Day Rainfall Forecast: