** Mixed and choppy has been the CBOT this AM with corn and soybeans trading on either side of unchanged, while wheat holds in the red. The volume of trade has been moderate with corn showing the best trade volume. Traders and producers understand that the harvest is dead ahead and that seasonally, CBOT prices tend to soften into late September or early October. As such, few are willing to be overly bullish with a positive USDA report on Tuesday unlikely to follow through to the upside. Combine results will be key to autumn price direction, but any big harvest activity is still several weeks away. Our bet is that November soybeans retest key support at $9.30-9.40, December corn at $3.45-3.50 and December Chi wheat at $4.25-4.30. Note that November soybeans fell below its 100 day moving average this AM at $9.5975.

** CBOT brokers estimate that funds have sold 1,000 contracts of wheat, 1,500 contracts of corn, and 2,400 contracts of soybeans. In soy products, funds have sold 1,800 contracts of soymeal and are flat in soyoil.

** US weekly exports for the week ending September 7th were; 26.1 Mil Bu of corn, 40.6 Mil Bu of soybeans, and 16.4 Mil Bu of wheat. The soybean export total was above trade expectations, while the grains were close to forecasts.

** WASDE is likely to raise their estimate of 2016/17 US corn exports by 75-85 Mil Bu based on strong late summer US demand. US 2016/17 US soybean exports could be raised 10-20 Mil Bu. WASDE won’t wait until the September Stocks report boost US exports based on the export data they have in hand. No change in US 2017/18 wheat exports is expected.

** FAS reported the sale of 352,000 MTs to unknown destinations this AM. China still has large October forward coverage to lock in and they hope for another test of the $9.20-9.30 support area to add to forward coverage.

** AgResource President Dan Basse has just returned from presenting at the Russian Grain Union meeting in Moscow late last week. The meeting was attended by large producers, exporters and importers. The new Russian ag minister assured the crowd that the Gov’t would do all it can to boost their export and storage availability to allow Russia to be a bigger future trader in world grain markets. Most at the RGU Conference expected that Russia would be able to export 32-33 MMTs of wheat and at least 5.5 MMTs of barley and 3-3.5 MMTs of corn. In the future, Russia will have massive carry-in stocks of grain and that farmers showed no willingness to curtail 2018 seeding amid sliding prices. Most Russian producers indicated that yield was more than offsetting the decline in domestic prices (profitability). Russia looks to expand their investment in rail wagons in the future and will continue to offer subsidies to move grain from the north. It will take a dire Black Sea drought to shift the world wheat price structure .

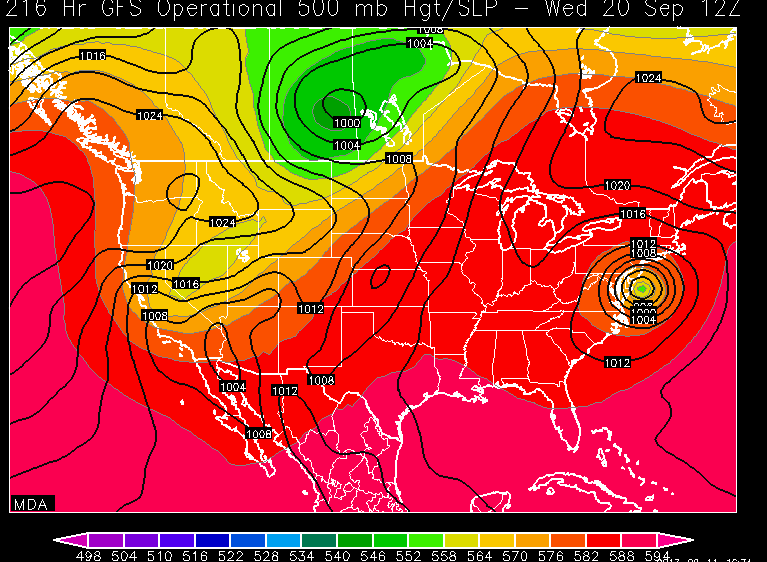

** Midday GFS Weather Model Update: The midday GFS is unchanged through the next 10 days – despite minor eastward shift to the path of Irma’s remains. The trend is wetter in the Plains & Midwest beyond September 21st. The model features a low pressure Trough in the Pacific Northwest which will allow for rains to work across the Dakotas, NE, IA, KS in the 8-15 day period. A pattern shift is occurring that offers some much needed rain ahead of US winter wheat seeding. Hurricanes tend to produce major US pattern shifts and Irma is offering such a change. There is no evidence of any Midwest frost/freeze threat for the next 2 weeks. Hurricane Hose looks to make landfall across the Carolina’s into into Washington DC as a cat 3 hurricane on Sept 20th. This system could impact the Eastern US shoreline and should be closely monitored.

** AgResource Market Comment: Traders want to push fast forward to Tuesday and see/gauge NASS/WASDE estimates. Argentine weather is dry for the next 10 days which will improve seeding conditions. Like August, the industry is hoping for a bullish USDA report and future trading opportunities. Our lean is for a slightly bearish report.

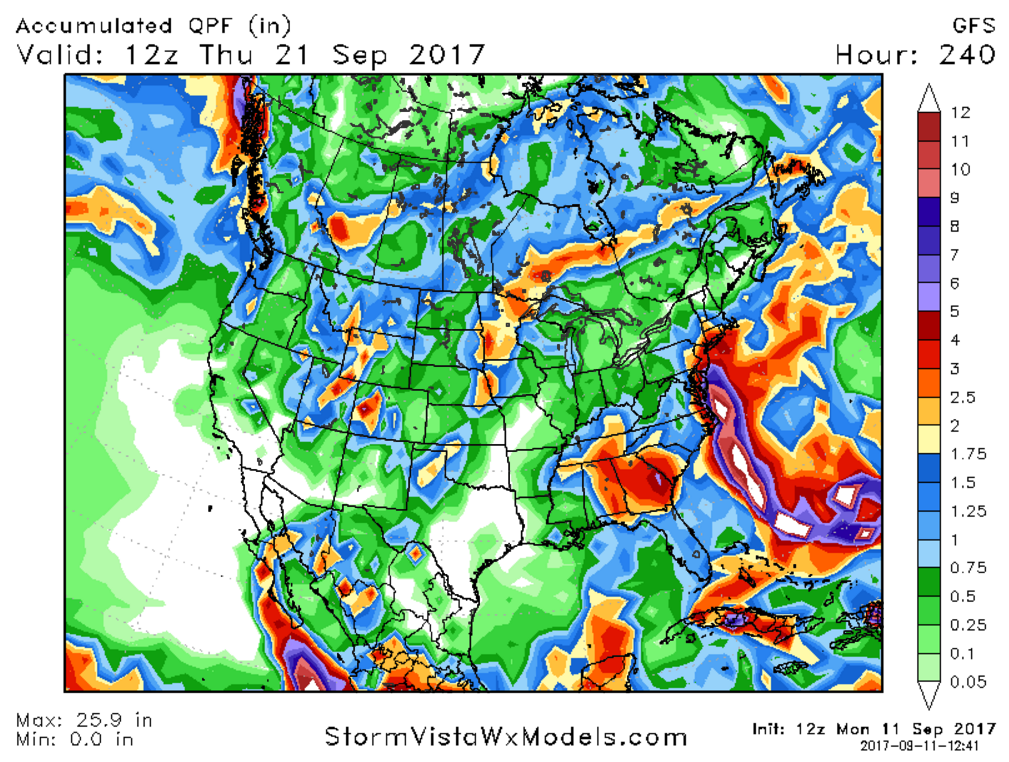

**10 Day GFS 10 Day Rainfall Estimate:

** September 20th Long Range Forecast: