** CBOT futures have spent the morning at firmer price levels with soybeans providing much of the bullish pull. November soybean futures have pulled above its early September highs at $9.775 and the 50 day moving average which triggered aggressive fund buying. Corn and wheat futures have followed with December Chi wheat testing $4.50 resistance and December corn holding last week’s low at $3.45.

The bears are surprised by the strength of the soybean market with values forming an upside reversal. The soybean charts will take a bullish turn with a close in November above $9.78. The bulls claim that the market was thrown bearish supply news that is already digested. ARC would note that if November soybeans close above $9.735 – the 50 day moving average – that additional buying will be noted going home.

** CBOT floor brokers report that funds have bought 8,000 contracts of soybeans, 4,000 contracts of corn, and 1,400 contracts of wheat. In soy products, funds have bought 6,000 contracts of soymeal and sold 2,000 contracts of soyoil.

** FAS reported that for the week ending September 7th (1st week of the 2017/18 crop year) that the US sold 11.6 Mil Bu of wheat and 41.2 Mil Bu of corn.

** The US also sold 59.2 Mil Bu of soybeans on the week – at the high end of trade expectations.

** For their respective crop years to date, the US has sold 469.4 Mil Bu of wheat (down 5 Mil Bu or 1%), 413.5 Mil Bu of US corn (down 257.6 Mil Bu or 38%), and 624.4 Mil Bu of soybeans (down 240 Mil Bu or down 28%). The US wheat export sales pace was a bullish surprise, while US soybean and corn export sales were a tad disappointing.

** The USDA reported that 198,000 MTs of US soybeans was sold to China this AM for the 2017/18 crop year. ARC is told that China has been an aggressive buyer this week covering their import needs into late October.

** Saskatchewan Agriculture reported that 65% of their crop has now been combined, up 20% from last week. This year’s harvest is well above the 5 year average of 40%. 63% of the spring wheat crop, 50% canola and 20% of the flax crop has been gathered. Commercials report varied yields with some extremely poor yields and some better. Most argue that a slightly further downward adjustment will occur in the October WASD report amid existing yield trends.

ARC would note that producers indicate that the window to seed winter wheat is quickly closing with producers unwilling to plant amid dry soils. Rain is desperately needed across the entire province.

** CBOT September futures cease trading today.

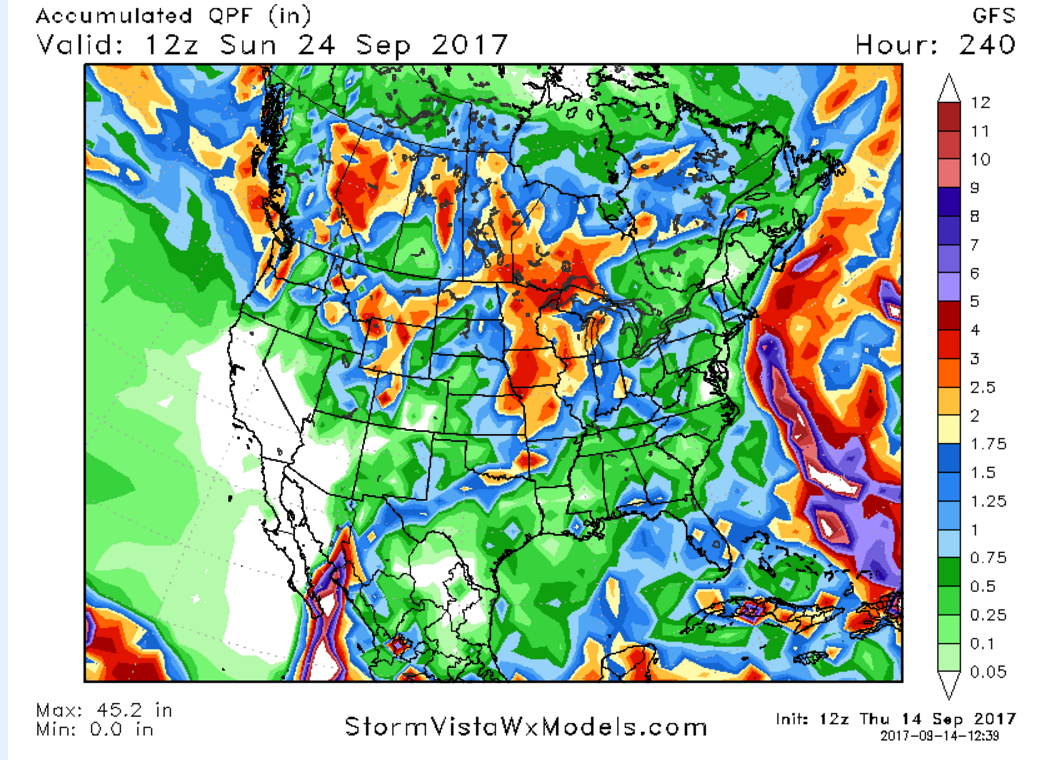

** Midday GFS Weather Model Forecast Update: The forecast is slightly farther south and east with heavy rainfall next week. This is based on a more easterly shift in the storm track of Hurricane Jose which holds across the eastern US shoreline. Heat returns mid next week as a high pressure Ridge builds across the Midwest as Jose nears the Eastern US Coastline.

The E Midwest and Delta hold in a mostly dry trend with temps averaging near to above normal. There is no indication of any frost/freeze looking into late September for the Central US.

The Brazilian 10-15 day weather forecast remains arid and warm into late September. The warm/dry trend looks to persist into early October.

** AgResource Market Comment: Harvest data will become more available in coming weeks, and the market will paying close attention to yield deviations from 2016. Early yields are down more than expected from last year and China has limited forward coverage. The marketplace will continue to listen to the combine (actual harvest data) with South American weather forecasts to gain in market importance going forward.

** 10 Day US Rainfall Estimate: