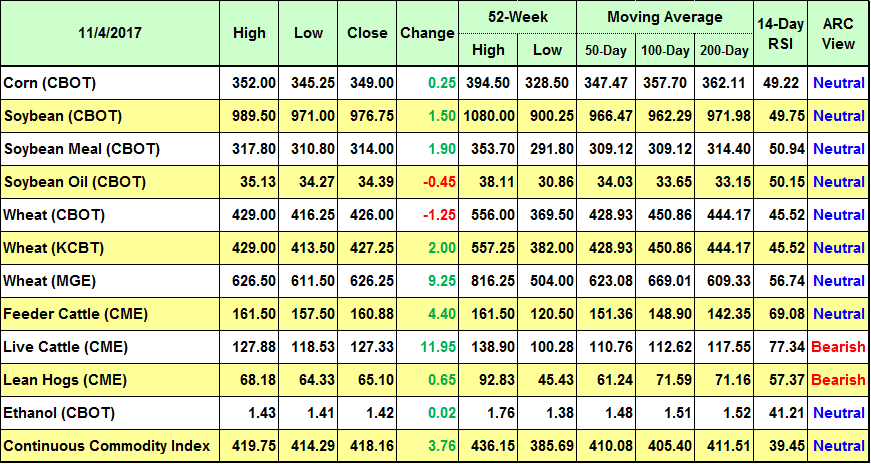

Commodity Index

The CCI/CRB index closed higher for the week and in doing so, confirmed a more bullish technical structure for world raw material markets. Crude oil has been pacing the commodity rally, which has pulled the CCI/CRB index up to its best close since April. The market continues to find support on world economic strength, and potential weakening of the US dollar based on a growing US budget deficit. ARC remains bearish on the greenback on a longer term basis, as GDP rates of emerging markets surpasses the US. The outlook for raw material demand is strong amid China’s ongoing investment in infrastructure with energy and industrial metal markets to outperform. ARC is turning bearish on US meat values, while the soy market is in a more bullish fundamental position. Use weakness to secure breaks.

Corn

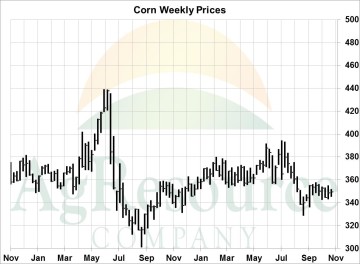

Dec corn ended the week fractionally higher. CBOT corn futures have spent the last seven weeks alternating between stronger and weaker closes – and have not traded outside a range of $3.43-3.59. This makes fundamental sense and ARC expects ongoing sideways price action into late Dec/Jan, when South American weather begins to have greater impact on yield. Corn support is a function of an excessive fund short positions which is near record large. Combine yield data, a much slower than normal harvest suggest the US corn crop is still 100-300 Mil Bu too low. The world feedgrain market is well supplied, but major exporter stocks are down slightly on the year. Simply put, any major move in price requires either very good or very bad South American weather. We caution against chasing breaks amid rising energy prices and the rapid development of La Nina. Rallies are selling opportunities and will remain so indefinitely as US acreage in 2018 will be higher. The only chance for a sustained CBOT corn rally rests with adverse South American weather.

Wheat

Wheat futures ended steady to a bit higher this week. World cash markets were relatively volatile, but Black Sea and Europe have maintained support at $192-193/Mt vs. $185/Mt on this week a year ago. Wheat still lacks a demand story, perhaps even more than corn & beans. The Southern Hemisphere harvest lies just ahead (progress in its in very early stages in Argentina), and yield/quality data there will be important over the next 4-6 weeks.

Black Sea exports continue at a record pace, and while the market there has been unable to rally, it’s also been unwilling to break. Most importantly, there’s no sign yet that any boost in US export demand is imminent, and so rallies in the near term will be limited to short covering. Notice that spot CME futures have so far held strong at a monthly uptrend line, but without threats to S American corn production, we doubt there’s much upside above $4.75, basis spot futures. Our bet is that a secondary seasonal low will be scored in early December.

Soybeans

Soybean futures spent most of the week trading higher on technical buying and fund short covering, but gave back gains ahead of the weekend. The Brazilian Real fell to a 4 month low against the dollar, and Brazilian farmers were quick to add to their new crop hedges on the currency break. Fundamentally, the November trade report showed that the US exported a record amount of soybeans in the month of September, and a strong export program is expected to continue into early 2018. However, the larger carryin and a record large crop will still leave December 1st soybean stocks at the largest on record. Technically, resistance in spot soybeans is expected on rallies back to $10.20 while support is expected on a break back to $9.50. We hold to a view of adding to sales on strong rallies, as a major Brazilian crop problem is needed to sustain a lasting bull market.

Cattle

It was a sharply higher week of trade in the cattle markets, with December cattle gapping higher at Monday’s open following strong gains in this week’s cash market. Cash cattle trade started slow at around $120, but moved to $124-125 late in the week. This took December cattle sharply higher on Friday.

Fundamentally, weekly cattle kills remain large and the outlook calls for record large beef production through the 4th quarter. However, cash beef and cattle prices have traded far better than expected (relative to production) on exceptionally strong demand.

The cattle markets have quickly traded through all fundamentally based levels of resistance, while the next technical targets for spot cattle futures are against the spring highs at $132-134. Looking ahead to next year, cattle futures for the 1st quarter are seen as fairly valued at $128-131.00 February, but June futures are overvalued above $120.00.

Hogs

It was a volatile week of trade in the hog market with all trading months (including December) marking new contract highs, with the CME trade drawing on continued cash market strength. The cash hog index finished the week at just under $70. Fundamentally, counter seasonal strength in the cash hog market has been surprising given the size of weekly slaughter rates. The cash market rally through October is reflecting exceptionally pork demand – domestically and at export. Both cash and futures prices have far exceeded historical fundamental values, and the CME hog contracts are all now exceptionally overbought. There is no change in the outlook for record production in the remainder of this year or the first half of 2018. Our view is neutral, though producers should stay mindful of the strong forward margins offered and use hedges on rallies.