Corn, wheat and soybeans have extended their overnight losses, and with wheat leading the way down ARC suspects much of this is currency/macro driven. The US dollar at midday is a bit higher, while all other major exporting currencies are weaker. Crude has been back and forth this morning but currencies have failed to respond to any energy rallies, and so there’s just no fodder available to encourage any new spec buying/short covering.

Brazilian corn export shipments were a sizeable 1.1 MMTs, with another 3.4 MMTs due to be shipped in the next several weeks. This is more in line with the USDA’s forecast, and ARC mentions Brazilian corn exports are likely to continue into the very early part of 2018. US exporters sold 135,000 of meal to the Philippines but otherwise no sales were reported. Weekly export inspection data has been delayed.

New weakness in Russia’s ruble has pulled down wheat replacement costs there to $154-155/MT, basis Southern Russia. This is a full $38-40/MT below this morning’s quoted fob offers. ARC still doubts much downside risk exists in world cash grain prices, but falling interior prices in Russia suggests rallies will be equally hard fought. Russian wheat continues to find demand at $192-194/MT, and last week’s modest rally in the US put Gulf HRW at a $10/MT premium to comparable Russian & German origin. Finding incremental world market share in both corn & wheat remains a slog.

There are also reportedly two cargoes of beans delayed at Chinese ports, citing a lack of GMO safety certificates. The trade is on high alert for any lasting slowdown of Chinese import based on recent gov’t protocols.

The US weather forecast is even drier in the extended period, but also a shade cooler. Pesky showers will continue across the Central and Eastern Midwest late this week and on the weekend, focusing on WI, MI and the mid-Atlantic where accumulation is pegged at .50-2.0”. Elsewhere, however, little to no precip is indicated through Nov 20-21, and temps, overall, will exist within a few degrees of average. The 2017 US harvest should be nearly completed in the next 10 days.

Interior US basis in recent days/weeks has been mixed, but generally is very weak across Plains & Western Midwest. Wheat basis has, on the margin, strengthened by remains upwards of 40-65 below spot futures, and with delivery on the horizon the trade anticipates either a lack of sustained rallies or large deliveries against futures. This has been a theme in the wheat markets especially over the last 12 months – weakness into delivery followed by modest recoveries during the delivery period.

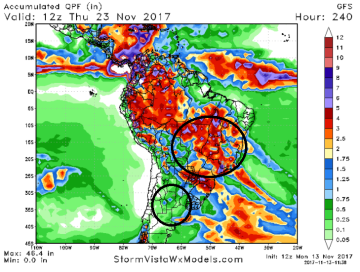

Midday GFS South American Weather Update: The GFS at midday is favorably wetter in Central and Northern Brazil, and a rather normal pattern of rainfall is indicated through the later part of November. It remains that meaningful precip through the week ahead will be strictly confined to Northern Brazil, though will include Mato Grosso. Thereafter, a rich monsoonal flow will impact the whole of the country. Precip accumulation in the 8-15 day period will range from 3-5”, spread evenly across Brazil’s primary soy belt.

We do mention that the forecast in Argentina has trended drier though, and aside from regionally decent rainfall in Cordoba next week a prolonged pattern of dryness will persist there. Fortunately excessive heat is absent. 10-day precip is below.

AgResource Market Comment: Near term crop supplies are large, particularly in the Western US Ag Belt, and this only changes with supply dislocation in South American this winter or the EU/Black Sea next spring. We advise against chasing breaks, but following the Nov WASDE – namely the 300 Mil Bu surge in US corn supply, even moderate rallies should be used to catch up on sales.