Commodity Index

The CCI/CRB index again traded in a narrow range, ultimately ending slightly higher. The rally occurred in spite of another slight boost in the US dollar, but positive expectations over emerging market growth are intact. Capping rallies this week were the loss of 33,000 US jobs, attributed mostly to this year’s series of devastating hurricanes. Crude ended the week below $50/barrel, though ARC mentions US crude/gasoline inventories are at/below year-ago levels, which is supportive longer term.

For ag markets, specifically, attention will be turning to Southern Hemisphere production and surpluses. Deep yield losses have already occurred in Australia’s wheat crop, and while it’s very early, South American weather in Sep and early Oct has been far from ideal. Whether world inventories of corn & soybeans grow or shrink in 2018 is still very much in question. We maintain that breaks in commodity prices will be short lived.

Corn

December corn fell 5 cents on an almost complete lack of fresh news, little change in South American basis, and as the rally in global cash milling/feed wheat prices paused. There’s little new to say about yield, with results still rather variable so far. Final yield should lie somewhere between 166-170, but fine-tuning this any further is difficult. US corn stocks will be plentiful, but increasingly the market will turn its attention to whether supplies in S America will be growing or shrinking in 2018.

It’s too early to estimate S American yields at anything other trend, but we do mention that the arrival of Brazil’s wet season is not indicated in the next two weeks, and so far seeding in both Brazil and Argentina is behind schedule. More attention will be paid to Brazil dryness should it continue into late Oct/early Nov.

In the near term there’s just not any compelling evidence to support a major move in either direction, and Dec corn is stuck in a range of $3.45-3.75.

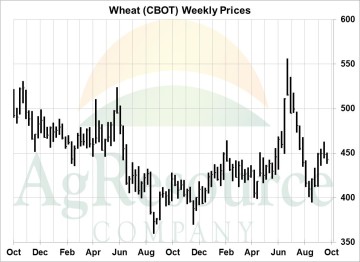

Wheat

US futures fell 2-7 cents, led by KC contracts, amid a pause in the Black Sea cash market’s rally and an otherwise dearth of market-driving news. Needed rain has also finally fallen across the US SRW Belt, which has been incredibly dry over the last 45 days, and US exports sales, which are inching higher, have been limited to mostly traditional destinations so far.

However, ARC maintains that breaks should be used by end users to extend wheat & flour coverage. Funds hold a sizeable net short position in Chicago. Problems abound in the Southern Hemisphere, where virtually no rain has fallen in E Australia in September, and Argentina is still plagued by excessive water across half its wheat belt. Seasonal trends in N Hemisphere cash markets point higher through late year, and we doubt the highs in Russian fob offers have been scored just yet. A range of $4.40-4.80, Dec CME, is projected, and much improved US export demand will develop beginning in early 2018.

Soybeans

Soybeans finished the week with modest gains, near the highs of the week. Support was offered by ideas that both futures and cash basis are in the process of forging seasonal lows, as well as anticipation that strong Chinese demand could surface next week. Crush margin estimates have turned positive in recent weeks, while estimates of domestic soymeal stocks have fallen since August. However, the main even for the markets in the week ahead will be the October crop report. Yield reports have been highly variable across the Midwest, ranging from record large, to 10 BPA under last year. The average trade estimate calls for no yield change in the October report.

Seasonally, it’s the wrong time of year to be bearish soybeans, as harvest lows are typically forged in the early days of October. Note in the chart that trend line resistance sits near $10, where we target our next sale.

Cattle

Cattle futures were on both sides of unchanged this past week and finished firm. December cattle started the week under pressure, but found support on Tuesday on ideas that this week’s cash trade would likely be no worse than steady, and the market traded higher late in the week. Initial cash sales developed around unchanged at $108, while beef prices also held around steady through the week. Weekly cattle kills remain exceptionally strong relative to the last several years, but the beef market has done a good job absorbing the additional supply, with strong exports noted in recent months. Seasonal demand is expected to offer support to the beef market on sharp breaks in the coming months, while larger cattle numbers look to cap strong rallies, all of which looks to keep cattle prices in a broad range of $105-108 on the downside, and $117-120 on the top end, into the end of the year.

Hogs

Hog futures closed higher for the week, but were well under early highs on late week selling. Weekly hog slaughter and pork production rates have been at record large seasonal levels, yet packers surprisingly were bidding for extra loads, which lifted the CME’s lean hog index and triggered the week’s rally in hog futures. Slaughter margins this week are estimated near $38/head versus $20 just 8 weeks ago, and packers are trying to keep plants full to capture margin. However, the September inventory report confirms that hog numbers will remain record large into the end of the year, and it’s doubtful that either slaughter rates have peaked or that the market has traded seasonal lows. Our view stays bearish, with spot hog futures expected to fall back to $50-55 within the next 6-8 weeks.