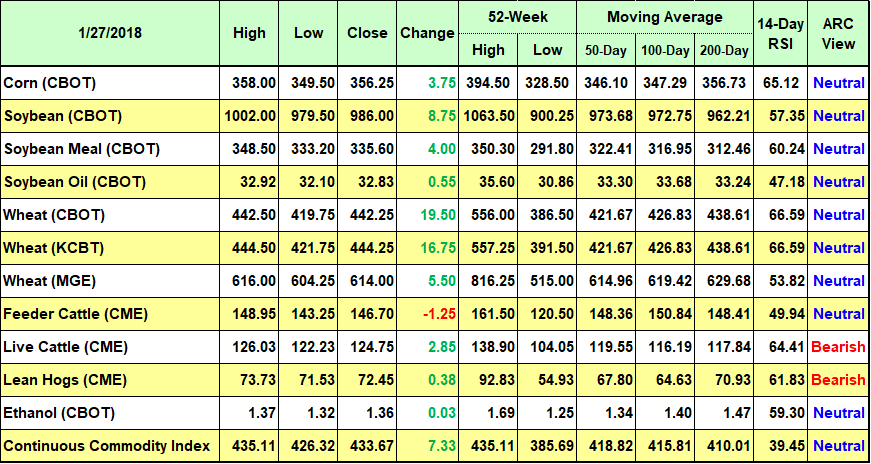

Commodity Index

The CRB/CCI Monthly Chart has confirmed a breakout and an end to the 7 year bear market in raw material markets. The attached chart reflects the new found trend that should produce a further rise in the index into the middle of 2018. A falling US dollar, sharp rise in emerging market import demand and a world awash in cash with reduced US tax rates has combined to fuel the commodity optimism.

The CRB breakout to the upside occurs at a time when fund managers are overly short of ag commodities. ARC research argues that the hefty shorts worry fund managers with the US greenback in fast retreat.

Moreover, ARC expects that President Trump in the State of the Union speech will argue in favor of a large US infrastructure spending – which will demand additional steel, energy and other raw materials.

AgResouce maintains a bullish broad commodity outlook and would be a buyer of corrections

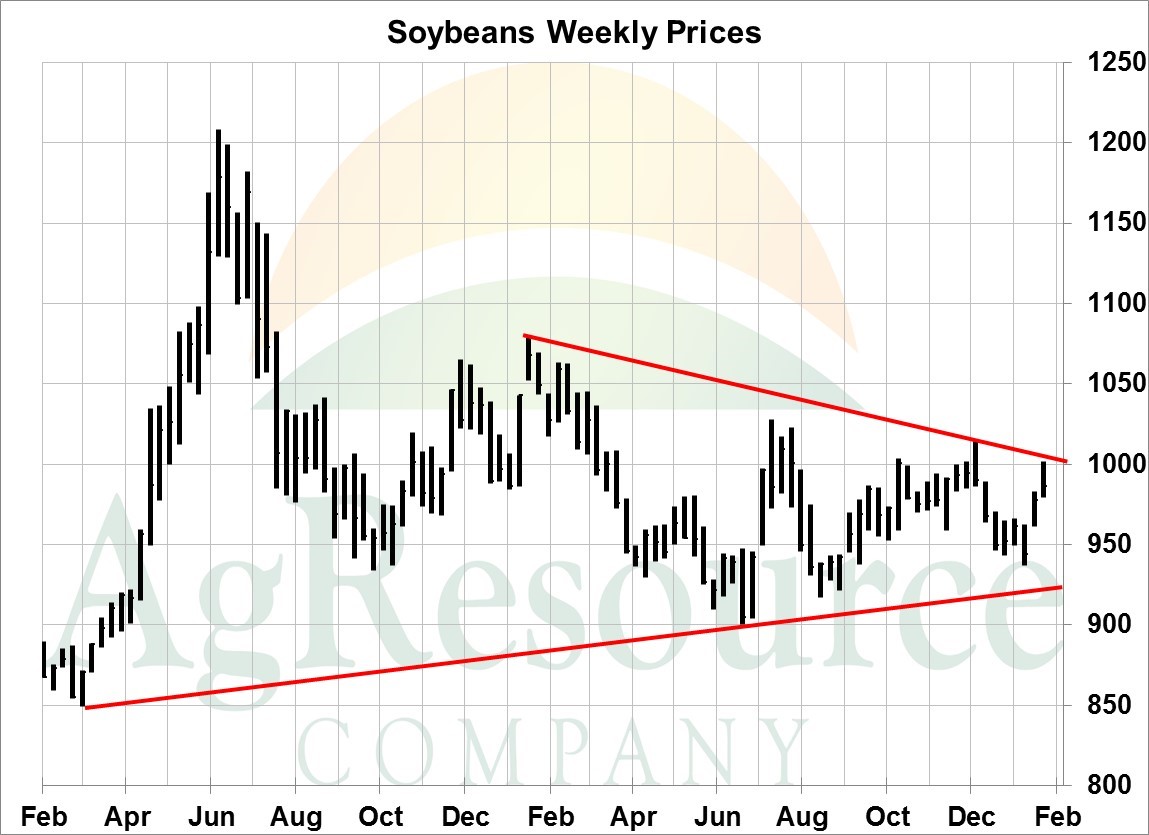

Soybeans

Soybeans traded higher through the week and were again lead by the meal market on concerns for the Argentine crops. Both soybeans and meal traded up to key resistance markers, and eased at the end of the week on profit taking, though both markets were still higher for the week at Friday’s close.

The Argentine weather forecast offers little relief for the driest parts of the country’s soybean crop. Limited rains and warming temps are offered through the first week of February, while longer term climate models show similar trends continueing to the end of the month. Funds are still holding onto a record large net short soybean position for January, of just over 80,000 contracts. Our view is that price risks stays to the upside until drought breaking rains develop.

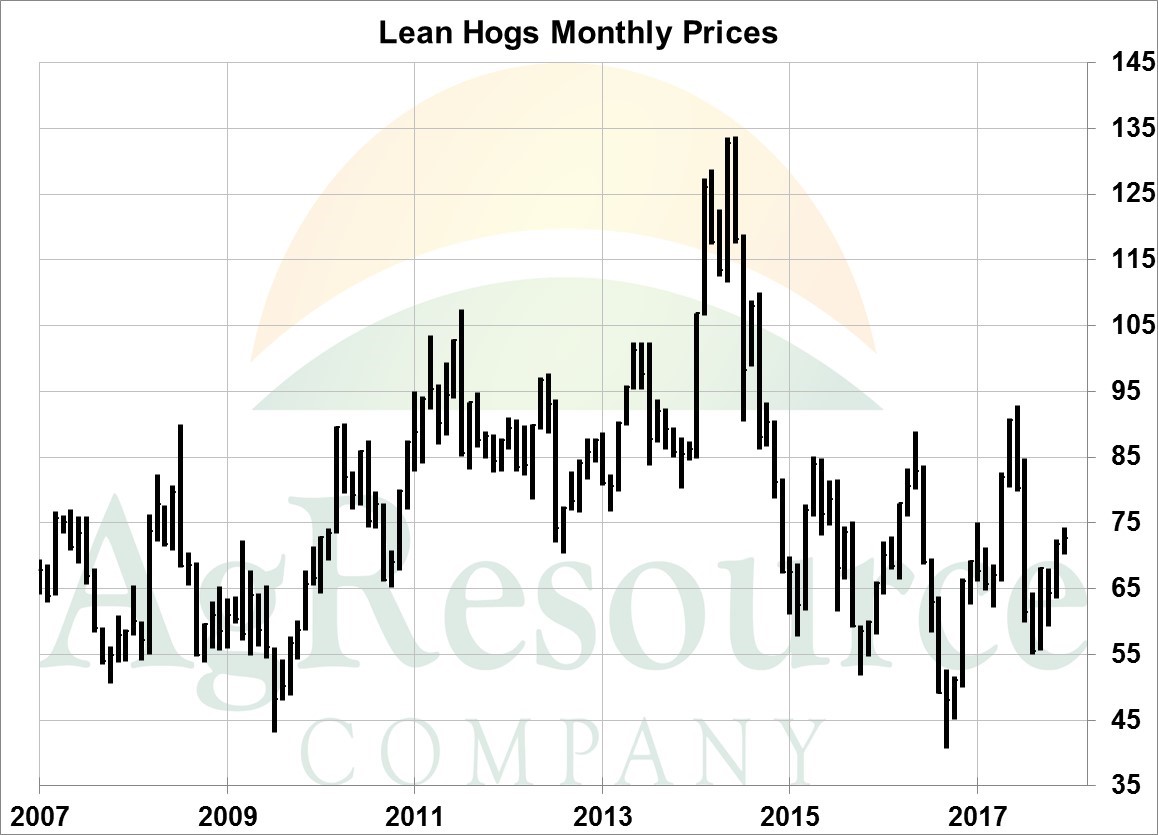

Hogs

It was a sharply mixed week in the hog market, with February trading on both sides of unchanged, while summer hog futures finished the week lower. February is now more closely tied to the cash market, which was held firm through the week, while rallies in summer prices struggled against an outlook for record large US pork production. Fundamentally, hog slaughter remains record large, and the cumulative kill total through January has been 7% bigger than a year ago.

Exports remain strong, but are simply keeping up with production, at least so far.

Technically, the hog market has held in a broad range over the last several years.

The short term trend is up on seasonal considerations, and our outlook for spot hog prices is for a broad range of $70-85 into the summer, and we continue to advise sales against summer production on strong rallies.

Corn

March corn rallied to new 7-week highs as meaningful rainfall has failed to appear in Central Argentina, and as weakness in the US dollar has maintained Gulf corn’s position as the world’s cheapest feedgrain. And amid concern over Argentine production, Gulf corn is the world’s cheapest feedgrain well into early summer, and weekly export sales will remain elevated in the weeks and months ahead. ARC’s work suggests that drought in Argentina is beginning to affect the 2018 world corn trade matrix, and also raises the importance of Brazilian safrinha production.

Broadly, we look for a measurable decline in US and world stocks via lost acreage and the arrival of La Nina, and a close eye needs to be kept on the coverage of severe/extreme drought in the US. It’s been tough to ignore the impact of La Nina on the world’s major corn growing areas. Corn has bottomed.

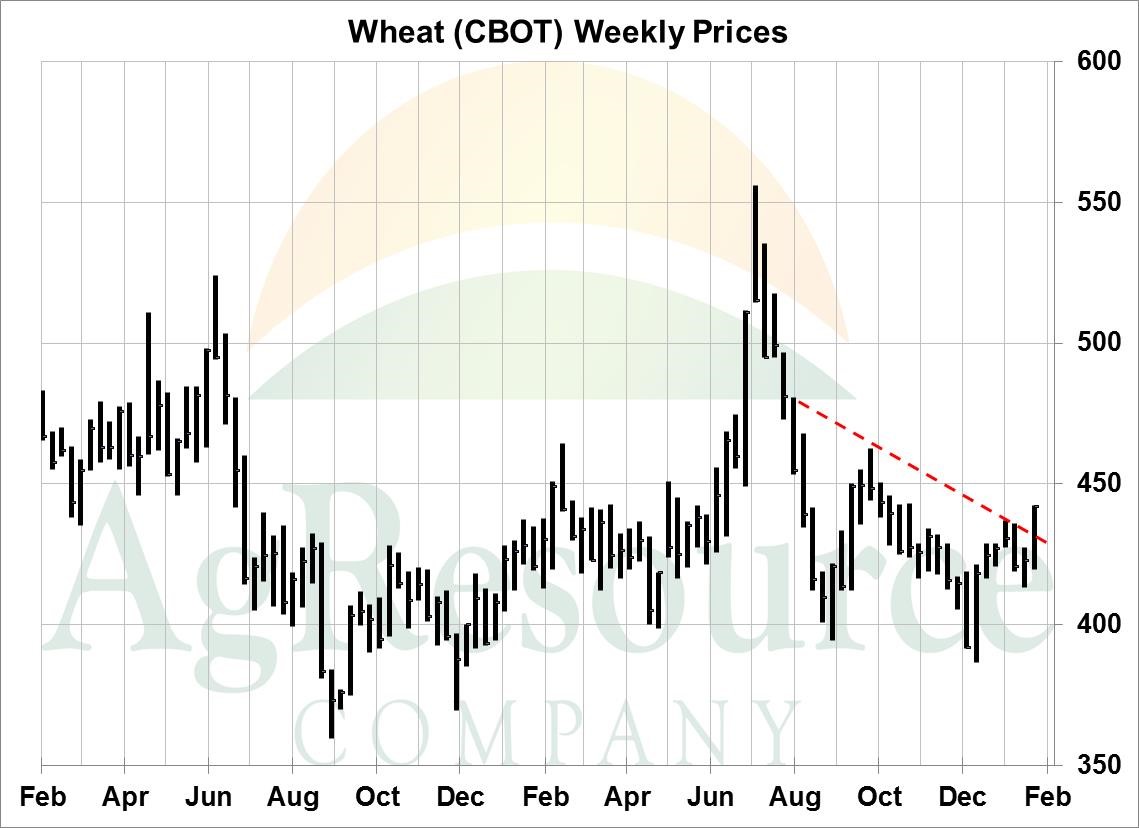

Wheat

Wheat futures rallied sharply amid additional short covering, new multi-year lows in the US dollar, and as it’s difficult to ignore the recent expansion in severe drought conditions across the Plains. Fundamentally, US & world markets will remain more than adequately supplied, but on the margin our work suggests a modest cut to world stocks, and potentially sizeable cut in the US. La Nina continues to plague the HRW Belt – it’s now been more than 100 days since it last rained in parts of TX & OK – and short and long term forecasts maintain well below normal precip into the end of February.

Unlike corn, which is benefitting from strong biofuel production, wheat still lacks a demand driver. Assuming normal weather in the Black Sea the US’s share of world trade will remain abysmal, but without better Plains moisture by March 1 a test of $4.75, March CME, is possible. Look to target $5.20, Dec CME, to extend new crop sales.

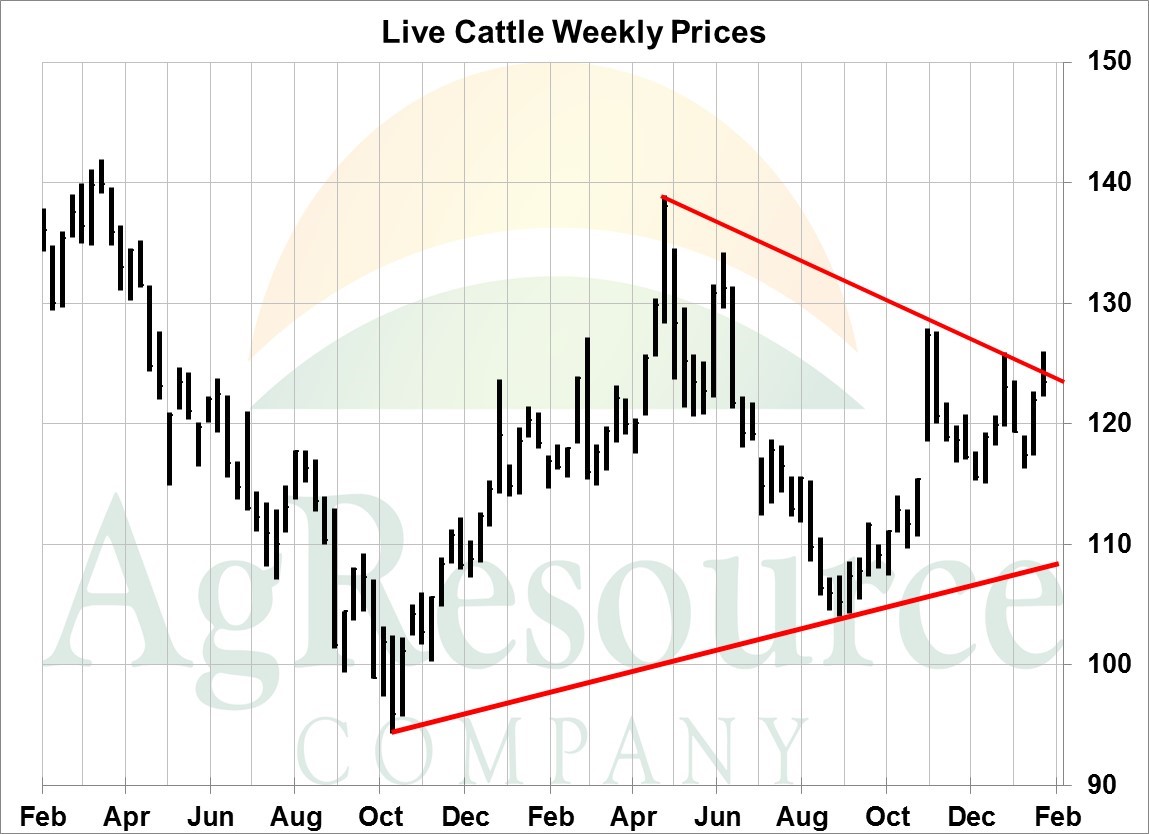

Cattle

It was a wide week of trade in the cattle market, that left futures well off the highs but still slightly better for the week. Strong demand developed at the start of the week on the previous week’s cash trade, and follow through technical buying. Prices continued higher through the week, but collapsed late Thursday, and then recovered some of those losses through Friday. Fundamentally, the market continues to struggle with uncertain demand outlooks versus increasing beef production forecasts. Record or near record production is expected in every quarter of 2018, so the supply outlook is bearish. What is unknown is whether the growing US economy will lead to stronger demand in the year ahead and support steady or higher beef and cattle prices. Technically, spot futures rallied through but closed back under a longer term down trend line. The On Feed report looked neutral to slightly bearish against expectations, but is likely to be trumped sharply higher late week cash trade at $127. Our view is that the CME is already pricing in a significant increase in demand through the 2nd quarter, and we continue to advise sales on rallies