Commodity Index

Commodity indexes finished slightly lower on the week, but did not take out the prior weekly low, keeping a bullish outlook alive. Crude oil prices continue to be supported by declining supplies and strong world demand. However, the late week rally in the US dollar offered resistance to commodity prices and the CCI/CRB Index declined. ARC maintains that higher prices lie ahead into the 4th quarter with funds likely to position long commodities with the spread between stock valuations and the commodities at a record high. One has to be careful about being too bearish commodities in the weeks ahead. ARC doubts that a US dollar rally can be sustained with US Tax legislation likely to encounter more than a few political speed bumps. US and world economic growth prospects look solid into 2018 and world raw material demand is growing rapidly.

Corn

CBOT corn prices ended the week lower on growing US harvest pressures amid reports of better than expected yields. It appears that the cool temps of late July and August played a large role in producing better than expected US corn yields. Another .5-1.5 BPA hike in US corn yield is possible within the November NASS report.

The close below $3.45 in December corn sets a downside price target of $3.30-3.35 in a retest of the September bottom that was scored during late August. ARC does not forecast even lower prices until the size of the South American corn crop is better known. Amid La Nina, the odds are high that there will be a few good weather scares during their growing season. Corn has another 10-15 cents of downside price risk before a secondary seasonal low is forged.

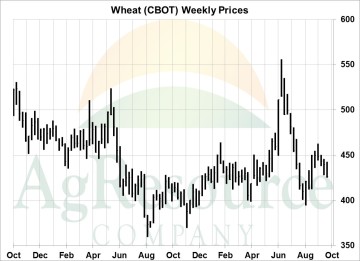

Wheat

US wheat futures closed lower as world fob prices started to retreat on larger than expected Russian and Ukraine exports during September and October. The large exports and weak domestic cash wheat market in the US has helped pull prices lower for the past 3 weeks. ARC research argues that additional weakness could be noted into 1st notice day against December futures. The oversupply of world and US wheat could produce a decline to $4.05-4.15 basis KC/Chi spot futures. Recent rains have helped stabilize the Aussie crop while planting in the US, EU and Black Sea has been uneventful. The key going forward will be winter weather across Russia and the amount of winterkill that befalls the crop? ARC research sees US wheat futures in a sideways range of $4.05-4.70 into spring.

Soybeans

It was a lower, but largely uneventful week of trade in the soybean market. After testing key resistance at $10 the previous week, the market turned lower on weak cash markets and building harvest pressure. Fundamentally, large US supplies are known while export demand remains exceptionally strong. Estimated Chinese crush margins are rising and China is expected to remain a strong buyer of US soybeans into early 2018. Technically, spot soybean prices failed at key resistance, and a close over $10 is needed to spark any significant rally. Most likely, the market is stuck in a broad range with export demand to offer support on breaks. S American weather looks to remain a dynamic with wetter conditions needed across the north and drier weather for Parana/RGDS. Midwest soybean yields are starting to fall off on the later planted varieties and a furter drop in the US soybean yied is expected in November. A sub 49 BPA US soybean yield is becoming a strong possibility. ARC’s downside price target is $9.70-9.75 November for a secondary harvest low in the week ahead.

Cattle

It was a mostly lower week of trade in the cattle market, with rallies struggling against lower cash cattle and beef trade, as well as selling ahead of the October Cattle on Feed report. Cattle slaughter and beef production rates continue to hold well above last year, and the monthly Livestock Slaughter report confirmed September beef production was the largest in 7 years, while the monthly Cattle on Feed report confirmed fed cattle numbers were at 105% of a year ago. The supply outlook alone is bearish for US livestock and red meat prices. However, demand appears quite strong with the choice cutout value trading $20 higher than a year ago. Spot cattle futures found support last week at $110, which is also where the week’s cash business began trading. However, the On Feed report looks to weigh on cattle trade early next week. Initial support is expected on a break back to $112-113, while late year rallies likely to be slowed by record large 4th quarter beef production. Sell rallies.

Hogs

Hog futures traded and closed higher for the week, with support coming from continued strength in the cash market and technical trading. Fundamentally, hog kills in October remain well above last year, while the monthly Livestock Slaughter report confirmed that the September hog slaughter was up 3% and record large for the month of September, and the 2nd largest 1 month hog slaughter total on record. Yet despite large production, the pork cutout is priced unchanged from a year ago, while cash hog prices are nearly $10 higher! Technically, December hogs have trended higher from mid-September and are still searching for a top, with the last remaining technical targets being contract highs at $65-66 (traded last summer). Given the magnitude of US red meat that will be produced in the upcoming months/quarters, we can not advise a bullish outlook. Relative to the supply CME hog futures appear to be overvalued; however the relative strength in cash prices shows exceptionally strong red meat demand. It’s the strong demand that is lifting valuations.